As the prize was sponsored by the Laudato Si’ Challenge, the theme of the Hackathon was “Chasing a Billion Dreams — Building uncommon apps for common people” and the guidance I gave at the beginning of the Hackaton was the seven categories of the Laudato Si’ Challenge.

Explaining the Laudato Si

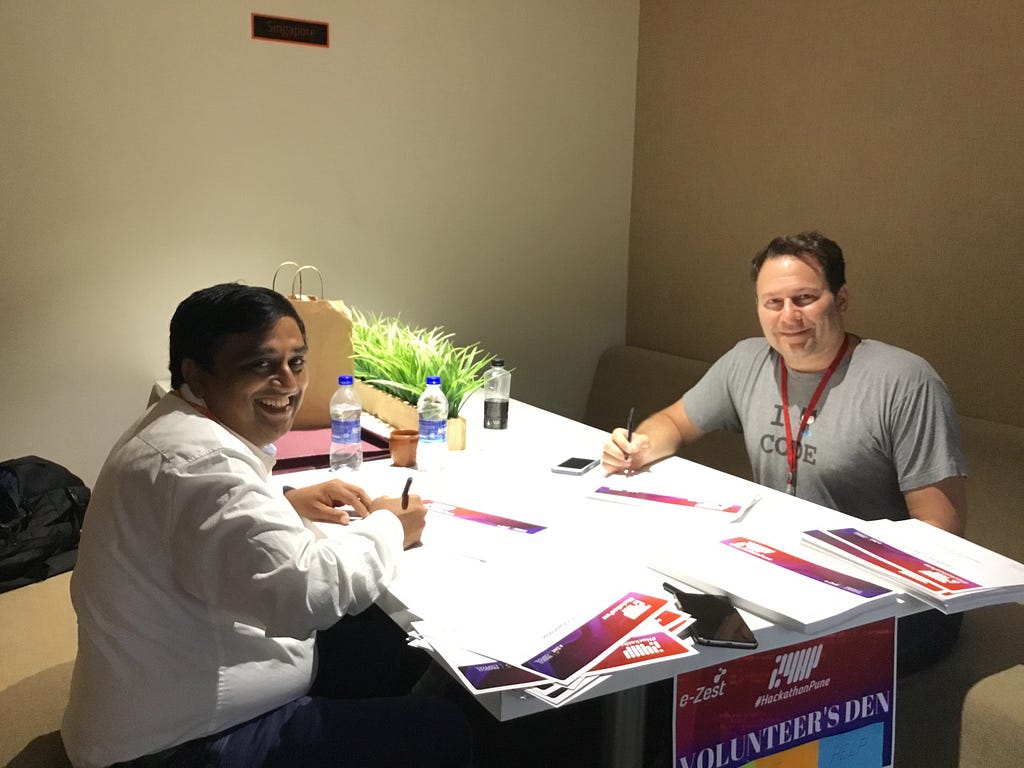

After we did the opening and set the ground rules, e-Zest CEO Devendra and I had to go and personally sign the 250 certificates of completion for the attendees. It took a while for us to sign all the certificates, but we had a lot of fun doing it. We joked and said this is what it must be like when the president takes office and immediately has to sit down and sign a bunch of stuff.

No event in India is complete without the certificate! 😉

As the day started to turn to night, I went to visit as many of the 100+ teams as I could. The standout teams to me where:

Emergency response: increase ambulance and police response time via location services, GPS, etc (the goal was to get an ambulance faster than an Uber)

Job and skill learning/improvement using machine learning (ML)

Augmented reality social media like Pokemon Go for social activists

Crop health app via image analysis of drone photos

Car lane sensor and software for the masses

A Firefighting robot

Wheelchair automation and navigation

Governmental services for the masses

Solar power installation chatbot

Farming automation and instrumentation via Industrial IoT

As you can see there was a healthy mix of software and hardware solutions. The trends were around some of the major problems in India: traffic, farm yields, competitive job market, and governmental services. It was great to see the Laudato Si’ values being implemented at a Hackathon in India.

We have a problem with not enough women in IT jobs in the United States. That is not the case in India: about half of the Hackathon participants were women. 50% of the winners at the Hackathon were women as well.

About 12 hours after we started, the developers started to get tired. That is when we took a break and had the live band come out and play. We temporarily turned the office into a nightclub.

Developers getting down

After midnight the sleeping bags came out and some people crashed for an hour or two. I was struggling with jet lag and cheated and went back to the hotel for about 4 hours of sleep.

Its not a hackathon without sleeping bags

At 6:30am the judges started to arrive and talk to each team, taking a few hours to narrow the field down from 100+ teams to a short list of about 10.

Final presentations

The final teams made their presentations and we chose the top three winners. While there was a lot of impressive hardware, all the shortlisted apps were software apps with the themes of: farming, social activism, governmental and emergency services, and traffic.

Besides having a lot of fun, we have three goals for organizing another Hackathon in India:

· Engaging with the developer ecosystem

· Learning about new technologies

· Seeing the Laudato Si’ in action

Engaging with the Developer Ecosystem

Spending a weekend side by side with the most motivated developers in an ecosystem for a weekend is best way to engage. We did the same last year and learned things that you can only learn by hanging out with the developers (what technologies they like, what technologies their customers like, how Agile is embraced, what companies are the best to work for, what companies are based in an area that is hard to get to, etc.) Looking forward to the full emersion experience again.

Learning about new technologies

Last year, we learned a lot about the bot market and hope to learn just as much as last year. This year the tech theme is a little more focused on Cloud, so we are excited about what kind of applications 150+ Indian developers will unleash. I usually find the most creativity at Hackathons and expect the same here.

For the last 200-plus years, capitalism has essentially been guided by one central tenet: delivering the most value to shareholders as possible.

Capitalism, of course, is not perfect.

So while companies scrambled to increase value for their shareholders, they did all sorts of atrocious things — forcing the government (or unions) to intervene on behalf of the citizenry.

In 1938, for example, the Fair Labor Standards Act became the law of the land, ostensibly outlawing child labor. In 1970, along came the Occupational Safety and Health Act (OSHA), which was designed to improve workplace conditions. The Family and Medical Leave Act became law in 1993, enabling workers to take extended breaks from their jobs for medical and family reasons without having to worry about becoming unemployed. There have also been laws passed to regulate the environment and prevent securities fraud.

The list goes on and on.

Focusing on the Wrong Thing

When companies are guided solely by maximizing shareholder value, management tends to focus on the wrong thing.

Capitalism, as it’s currently conceived, is far from perfect. Something needs to change — and everybody understands this.

This is why Bernie Sanders and Donald Trump — who actually had very similar messages — were so popular last election cycle. Both were a reaction to what is broken with the traditional model.

Capitalism is great — don’t get me wrong. But the misguidedness of focusing exclusively on maximizing shareholder value is what is broken.

Here’s where Bernie and others at war with capitalism get it wrong: Instead of focusing on the entire philosophy, they should be focusing on the shareholder value part of the equation.

Capitalism 2.0

I believe we’re in the middle of a defining moment. Capitalism is evolving into what I call Capitalism 2.0.

Capitalism 2.0 is straight up capitalism — but with a twist. Instead of focusing solely on shareholder value, companies operating under this model will prioritize the customer experience first and their contributions to society second.

By focusing on these two areas, shareholder value will automatically increase.

Thomas Malthus was the original proponent of the notion that there will be no jobs and no food in the future — and he made this prediction all the way back in the late 1700’s.

However, his wasn’t a prophecy of intelligent robots stomping out the little guy, but instead a commentary on the impending economic juggernaut that was the machine age.

“The industrial revolution will automate all the jobs and nobody will have anything to do!” he said. And really, can you knock the man for his anxious foretelling?

Back in the 1700’s, farming was virtually the entire economy. If they calculated GDP, farming would have been like 90% of GDP. Our friend Thomas was just reading the writing on the wall. His only mistake was being epically, embarrassingly wrong.

The industrial revolution was the greatest job creation engine of all time.

It created jobs that were unimaginable only 30 years earlier — much in the same way that Web Designers, Growth Marketers, and Data Scientists, were all unimaginable occupations 30 years ago. In fact, so many people all over the world switched from farm work to industrial work that today, farming isn’t a factor in a developed nation’s GDP and is left out of unemployment statistics. It literally got written out of the books.

Time marches on though.

Now we are exiting the Industrial Revolution and teetering on the cusp of truly entering the Information Age, a brand new era powered by connectivity and this big group of little people you keep reading about called Millennials.

Now sure, self-driving cars will eliminate the taxi (and Uber) driver, and machine learning will take away software developer jobs. Robots will serve coffee, iPads will teach our children, and I’ll be able to use a tricorder instead of going to the doctor. These are the things we’ve been promised.

So nobody will have a job in the future, right?

Well, hang on.

Just as our farmer from the 1800’s couldn’t have imagined the factory that he’d be working at in the next decade, or how someone from the early 1900’s couldn’t have imagined how the auto and aviation industries would dramatically shrink the world, or even how someone from 2000 couldn’t have imagined the digital marketing jobs that exist today, we similarly can’t imagine the jobs that will exist in 25 or 50 years.

The Information Age will usher in more jobs than humanity has ever seen before. We just don’t know what they will be yet.

Keep in mind though, that these jobs will come in a cycle — as they have for centuries. First jobs will be lost, and then they will be replaced a few times over. The magnitude of this progression is dependent on how disruptive the technology is — and AI, robotics, machine learning — these things are going to be exceptionally disruptive.

So sure, in the short term we will witness tremendous pain. We already are to some extent, and it’s causing a great divide to open within our country, and around the world.

Just as a laid off coal miner in Pennsylvania or an unemployed auto worker in Detroit can’t move to Silicon Valley and fill the open engineering roles out here, unskilled labor in central Britain can’t move to fill the tech jobs in London.

What do these things (partially) lead to? One has orange hair and the other has made it way cheaper to travel to England.

So yes, there will be tremendous upheaval of the status quo as we transition away from jobs that have sustained many over the past century — and those people will need assistance, not just financially, but also emotionally. Furthermore, they will need a new education to bestow them with the skills required to be competitive in the new economy.

Nevertheless, in the long term — say 50 years from now — we will look back and see that the Information Age was not the harbinger of humanity’s gainfully-employed doom, but instead a revolution that went on to become the new most powerful job creation engine of all time.

Capturing the view from Mori Tower, Roppongi Hills, Tokyo (Photo credit: Junko Nagao)

Since I moved to Japan over a year and a half ago, almost every business meeting I have had starts the same way. We file into a room, smile politely at each other, parade around the table to exchange business cards in the proper order, we sit down in our prescribed seats, and then there is an inevitable moment of awkwardness, followed by a perplexed stare, alternating between me, my Japanese colleague, and my business card.

In Japan, being polite, particularly in a business context, is of the utmost importance. I know people are not trying to be rude. I’m used to it by now, and I can’t blame them. I know I am unusual. The first question they ask is usually to slyly confirm that I am actually a Managing Partner of Fresco Capital. Given my age, my gender, and my most obvious foreign-ness, the fact that I am sitting across from them as an equal is undeniably shocking. The reactions are always entertaining — some are delighted, some are clearly offended, others in complete denial.

The first few months of this, my cheeks would burn in embarrassment as I responded politely to confirm my position and deliver the introduction of Fresco Capital, my heart filled with pre-emptive defensiveness and the chip on my shoulder aching deeply. Now, I revel in the routine and am grateful for my ability to use their response as a strong filter for potential partnership. You have to be open and curious to new things to find success in the world we live in today, and here I am, able to gauge that within the first thirty seconds of a meeting. Lucky me.

Then, comes their real question, accompanied by a puzzled brow and a heavy air of anticipation: “Allison-san, but why are you in Japan?” I used to dread this question, because just like anything in our quickly advancing world, the answer is complex and there are an infinite number of ways I could reply, most of which would not be relevant or appropriate for a business context. So, I experimented with different responses, carefully gauging the subsequent temperature of the meeting given a certain response, and attempted to rapidly iterate my way to a productive answer. At least I learned quickly that sarcasm is not well received here.

Connecting the Dots

“You can’t connect the dots looking forward; you can only connect them looking backwards. So you have to trust that the dots will somehow connect in your future. You have to trust in something—your gut, destiny, life, karma, whatever.”

— Steve Jobs

Reflections at the Imperial Palace, Tokyo.

Part of the problem was that, until very recently, I honestly didn’t have a full picture as to why I believed so strongly it made sense for me, and for Fresco, to set up our first new global office and team in Japan. Sure, I had an intense personal attraction to Japan, as well as a strong “Spidey sense” that there was a big opportunity for us to be one of the few global VCs in Japan. And whether it comes to people, investments, or partnerships, I’ve learned to trust my gut.

When we decided to bring Fresco to Japan, the dots looked a little bit like this:

Pros:

I’ve wanted to live in Japan since I was ten years old, when I made a best friend at summer camp who was from Tokyo. She started teaching me about Japan, and I was hooked. I tried to move here after college, but couldn’t make it work, and ended up going to Goldman Sachs in New York City instead.

I love sushi more than anything else in the world. Seriously, though.

We were just starting to raise a new fund, and there were interested investors in Japan.

My partners were keen to expand our global presence and set up a new international office.

Our portfolio companies were interested in expanding to Japan, or were already beginning the process, but needed help.

My then-fiance’s employer asked him to move to Tokyo and long distance sucks.

Cons:

My then-fiance became my ex-fiance, which was sad and embarrassing and very clearly crossed off more than one of the pros.

As a result, I knew exactly zero people in Japan.

I hadn’t spoken Japanese in nearly ten years.

After finally building our reputation in Hong Kong and China, we would be starting from square one, yet again.

Now that I have been in Japan for a year and a half, we raised a fund from Japanese LPs, I built a team of the most intelligent, forward thinking, and well connected Japanese partners, and we have brought four of our portfolio companies to Japan, I am starting to see the dots crystallise into a critical pattern that clarifies that initial gut feeling of why I and Fresco and need to be in Japan right now.

So, Here’s Why:

Our role as venture capitalists and my personal role as a trailblazer and explorer of the unknown is to create the future. We are living in unprecedented times, and the ways of building value in the past are no longer working. Our personal lives, our governments, our corporations, our jobs, and our infrastructure are being transformed by fundamental shifts in demographics, technology, and globalisation. Consequently, these key trends are shaping the period in which we live, and Japan is the first country in the world delicately poised on the precipice of these changes, reluctantly forced to navigate this complex but critical new era.

Just what are these critical shifts how are they playing out in Japan?

Reflections at the Imperial Palace, Tokyo.

1) Demographics

As a society, we created a series of formal structures to help individuals navigate their lives on Earth. These include the construct of marriage, a formal education system, corporate careers, pensions, and healthcare. Today, people are living longer, women are economically empowered, birth rates in developing countries are declining, and the Baby Boomer generation is retiring. These trends are forcing us to re-examine how and why we plan our lives and redefine the social and political structures that we have traditionally relied upon.

Japan is on the cutting edge of this trend. Long known for their health and long life expectancy, a child born in Japan today has a 50% chance of living to 109, the longest in the world. Simultaneously, birth rates in Japan have declined and the overall population is now declining at the fastest rate globally. Every year, Japan sells more adult diapers than baby diapers. How will the jobs market and government infrastructure adapt? A retiring generation of Baby Boomers is dramatically stressing pensions and healthcare, which were previously predicated upon an assumption that the current working population could support retirees. How will the country cope and how will infrastructure need to transform to support these unexpected trends? I don’t know, but we will soon find out.

Shibuya crossing, photo credit Daryan Shamkhali

2) Urbanization

As outlined in The 100-Year Life, “We are quietly witnessing the most extraordinary migration that humanity has ever experienced… from the countryside to the city.” In 2010, 3.6 billion people lived in cities, but by 2050 that number will be 6.3 billion. This is changing the shape and needs of urban infrastructure, and technology pays a key role in creating efficiencies that did not exist before.

Ueyama, Okayama. Rural areas have been hit hardest by the stagnating economy.

3) Stagnating Economic Growth

After the Great Financial Crisis rocked the US economy, then Europe, then the rest of the world, we have entered an unprecedented time of economic stagnation. Governments have responded by cutting interest rates to near-zero, and this has impacted the growth and development financial markets, savings rates, inflation, and GDP growth. Though the US and Europe are only now starting to grapple with the long term effects of these policies, Japan has been plagued by these trends for years and is now being forced to find new ways to climb out of its economic rut.

Vending machines and advertisement for the Robot Show, Shibuya.

4) Technology & Automation of Jobs

The internet is a relatively recent invention, but the change it is bringing on the world is accelerating rapidly. Personal computers have democratised access to information and resources, and social networks have opened up opportunities and connections that were previously seen as proprietary. Technology has impacted or been integrated into all products and services, and in this sense, every company is now a technology company in some way. As a result, every job is now a technology job, many jobs are now being automated or replaced completely, and new jobs are emerging on an hourly basis.

Both historically, with the automation of the manufacturing process, and socially, with the Japanese cultural fascination with robots, Japan has adapted and even embraced automation unlike any other country in the world. With a generation ready to retire, Japan is in a position to remain a thought leader in this sense. By 2060, the population in Japan is expected to be 87 million, a dramatic reduction from a high of 127 million. As stated in the 100-Year Life, “rather than worrying that robots are going to take our jobs, we should be delighted that they are arriving just in time to boost a flagging working population and maintain output, productivity, and living standards.” Indeed, if there is anywhere in the world where that may be true, it is Japan.

The Olympics are forcing Japan to think more globally.

5) Globalisation

As evidenced by the refugee crisis in Europe, global trade, the outsourcing of jobs, the current proliferation of cyberattacks, shifts in commodity prices, and the increase in correlation of global financial markets, the world is more connected than ever. People are scared, national identities are being threatened, and politicians are struggling to figure out how to adapt. As evidenced by Brexit, the election of Donald Trump and the subsequent impending reality of a wall, we are now facing resistance to globalisation in the form of isolationism and anti-immigration policies.

Though it remains to be seen how this will impact the US or European economy, for better or worse, this inward-looking, nationalistic approach is not new to Japan. The impact it has had on economic growth and innovation is alarming, and with the 2020 Olympics looming, Japan is now facing a critical moment where its leaders are seeing that opening up to the rest of the world is the only option. Again, what this looks like and how Japanese society, culture, and the economy will adapt remains to be seen. But the time to find the answers is now.

Conclusion: An Era of Questions

“Be patient toward all that is unsolved in your heart and try to love the questions themselves, like locked rooms and like books that are now written in a very foreign tongue. Do not now seek the answers, which cannot be given you because you would not be able to live them. And the point is, to live everything. Live the questions now. Perhaps you will then gradually, without noticing it, live along some distant day into the answer.”—Rainer Maria Rilke, Letters to a Young Poet

The view of Mt. Fuji from Yamanaka Lake, Yamanakako

More than ever, the future is plagued by questions. How will we, as both individuals and societies, adapt to these critical shifts in the the fabric of our world? What will the future look like and what role should we play in creating it? Many people travel the world looking for answers. What I have learned is that, thanks to the internet, Google, and good old human egos, answers are everywhere. However, given the complexity and interconnectedness of this next stage of growth, none of them are fully relevant.

My raison d’être in Japan is not to find the answers — because, there are none (yet). More importantly, living and working in Japan is forcing me to face and engage with the most difficult questions facing our generation. Just like I had to iterate my way to the proper response to, “Why am I here?”, Fresco’s presence in Japan is allowing us, our partners, our investors, and our portfolio companies to test solutions at a pace not possible anywhere else in the world. Hopefully, what we discover together will prove to be one of the most valuable exports Japan has ever seen.

For the last 15 years or so, I’ve been making the trek to the Consumer Electronics Show out in Las Vegas every winter. It’s where all the coolest next-generation gadgets and technologies are showcased.

I just got back from CES 2017 and I have to say it was one of the most exciting events I can remember. There were more than 177,000 people at last year’s event, and if I had to guess, I’d say we beat that number this year.

If you’ve never been to CES before, let me try to paint a picture. Events are scattered all across the city. But no matter where you wind up, the geeks hang out in the back showcasing their wares in small booths while the brand-name companies (e.g., Samsung and Sony) set up shop up front in larger booths.

That being the case, it appears the Internet of Things has finally become mainstream. This year, the IoT booths moved from the back of the room to the front of the room while VR and AR technologies were all over the back booths this year. We can expect these nascent technologies to make it to the front over the next few years as they develop further.

CES continues to attract more and more folks from around the globe. This year, there were more foreign entrepreneurs, investors, and professionals at CES — from China and Japan in particular.

There were also a number of other themes I picked on over the four-day event.

Smaller Companies Turned Out

At an event as large as CES, you obviously expect to run into the Amazons, Nikons, and Sonys of the world. (e.g.Nikon Project Helix)

They’re still there. But nowadays, the smaller booths are filled up by companies located all across the world. This year, companies from (not surprisingly) China and (surprisingly) Paris appeared to have spent the much money to showcase at CES.

Having all of these smaller companies with cool little products is great. It’s not every day that you’re able to check out an ozone ionizer that you can stick in your shoe to get the smell out. Or take a 3-D body scan and get a five inch 3-D printed version of yourself.

Fifteen years ago, that kind of product wouldn’t have a chance at CES. Today, they’re everywhere. What is more important is that they are not even in production yet, just a small batch run and now taking pre-orders or publicizing their Kickstarter. This wasn’t possible, even five years ago.

Car Manufacturers Prefer CES

The future of the car seems to hinge on technology.

Cars were everywhere at CES this year. There were connected cars and autonomous vehicles. Car manufacturers appear much more interested in releasing cars at CES instead of at the standard auto shows. They’re not going to the Detroit Auto Show to launch a new line; they’re coming to Vegas and doing that at CES.

All of the big name manufacturers — like Ford, BMW, GM, and Volkswagen — made the trek to CES. Of course Faraday was there, but more importantly, they took 64,000 pre-orders at CES for their $200k that is only in the concept phase. Even compared to last year, it was very apparent that technology is taking over the automobile industry.

The IoT Was Really Everywhere

At CES events in the past, IoT booths were all about mesh networks and sensors. Today, we’re seeing sensors in consumer products.

Everything is connected. There was even a connected hairbrush, which is the epitome of an unnecessary connected device. Still, products like that are great because in the coming years, the market will push out unnecessary devices. It’s just a simple issue of supply and demand.

Samsung — which has successfully shaken off its Note 7 debacle — was all the rage at CES. They built an entire connected kitchen which was completely mobbed. Everything was connected to the point we literally thought everything was connected. Unfortunately, the sink wasn’t connected — which we were kind of bummed about. It is silly. But if everything else is connected. . .

Thank You, Alexa

Alexa was truly everywhere, too.

Amazon opened up its API, and have manufacturers very obviously jumped all over it already. It bears repeating: Alexa was everywhere. Amazon even found a way to partner with physical buildings and futuristic robots.

Amazon made a huge investment in Alexa, which has already found a home in a number of IoT applications. In essence, Alexa is now the interface for all IoT devices that connects everything together. Who knows what the future will hold?

There are so many startups working on AI, AR, and VR. I am expecting to pursue an enormous selection of small batch manufacturers working with these technologies in 2018.

Some people think venture capital is just fine and doesn’t need to change. Others want to turn it into a hyper liquid automated platform.

It’s time to call bullshit on both views.

Traditional venture capital needs to be transformed and the process will happen one person at a time.

I gave a presentation to a group of family office investors and corporate investors about the “Do’s and Don’ts of Venture Investing” earlier this year using martial arts training as a metaphor. It covers a lot of basics, with details here and here.

The discussion below starts with some of the traditional issues around risk and return, then moves on to ideas about how to transform venture capital.

At the black belt level, the emphasis shifts to higher level training, including awareness of self and the environment.

A typical mistake for a beginner in karate is to punch before stepping. This results in no power — as we learned in brown belt, strength starts from the bottom and flows upwards. It seems easy which why it’s actually difficult and in fact many people simply don’t even notice the mistake. Even with the incorrect technique, it still feels correct.

Getting the timing right in venture investing is similarly a challenge. The biggest mistake is to sell too early. The only thing worse than missing out on a billion dollar investment is being an early investor and then selling out to a new investor for a small profit and missing out on the much bigger gain. I know of one investor who came in very early into Alibaba only to sell soon just to get the money back because of concerns about risk. Whoops.

Of course, there are certain situations where it’s better to sell. This can happen especially when a wave of lemming behaviour overcomes investors to jump into a theme.

There’s no formula for getting the right timing to sell, but compared to all other investments venture capital is about long-term returns, so you should be thinking in terms of years and decades, not day trading.

The foundation of looking at the risk vs. return over time is to always evaluate decisions as if you were investing for the first time. In reality, that’s difficult in venture capital because of the knowledge built up over time after an initial investment and the overall lack of liquidity. Still, it helps to set the right framework. A more detached assessment of risk vs. return tends to lead away from binary all or nothing decisions and towards a more measured approach.

Of course, the process is not all about numbers. In fact, understanding the motivation of founders, other investors and of course your own goals is critical. If the company has been grinding it out for 10+ years and everyone is ready to move on, it may not matter that the best financial decision would be to continue for another 10 years because from a motivation perspective the journey has finished. Conversely, if the company has just received a lucrative M&A offer, this might be just the catalyst for a highly motivated founder to push for a more aggressive scaling up strategy and reject the early exit. Human inputs can be the most important factors when it comes to evaluating risk vs. return.

People are surrounded by external distractions. In addition, our minds are constantly creating internal distractions. This noise stops us from concentrating.

One description of traditional martial arts is “moving meditation”. Embedded in this description is the idea of having an empty mind. The first step is to navigate external distractions. The more difficult challenge is to manage internal distractions. Rather than trying to push the distractions out of our mind with mental energy, which is impossible, the training emphasizes acknowledging distractions and then being able to let go of them. Empty mind is not a static state of being, it is a dynamic process.

At first glance, it seems ridiculous that an empty mind would be an important skill for venture investing. Traditional wisdom suggest that experience, especially domain expertise, is necessary to be a successful venture investor.

The problem with experience is that it is actually one form of noise. The deeper the experience, the louder the noise. If you have 23 years of experience building microcomputers and some kid comes along with an idea for a personal computer, all your experience screams “impossible, no way this will work”. If you’ve spent all your career selling packaged software and someone suggest selling software for a monthly subscription, your instincts react immediately that customers simply wouldn’t trust software that they don’t own. If you’ve built billion dollar satellites and a young team proposes to create a network of cubesats, the first reaction is to treat it as a toy project. That’s the voice of experience speaking.

An empty mind allows even experienced venture investors to stay open to new opportunities. You can’t ignore your experience — those thoughts will always be there. Instead, acknowledge them, let them float away, and then let your empty mind stay open.

The common assumption is that martial arts focuses on fighting. But upon closer inspection, there’s a clear emphasis on peace by many traditional martial arts teachers. Fighting is the last option of traditional martial arts.

Many startup founders and venture investors make heavy use of war and sports metaphors — destroy the competition, hunt down customers, don’t be a loser.

Words and metaphors influence behaviour and actions. So by definition people being led by these words will be approaching the world with at zero sum perspective. For them to win, others have to lose. Zero sum thinking implies a lack of new value creation. If you believe that technology is supposed to create new value, not simply take value from others, then by definition these zero sum metaphors should be rejected.

Of course many others will continue to view the world from a zero sum perspective no matter what you do. Instead of wasting your energy on constantly fighting with them, focus instead on partners who you can trust.

Trust is much easier to build with aligned incentives and shared values. Aligned incentives alone may not be enough if the partner is going to find a way to cheat at the first opportunity. Shared values create great intentions but without aligned incentives, there may be no tangible outcomes. So it’s important to have both.

The right partners will help you reach your goals faster no matter what games others are playing.

Reaching a black belt level in traditional martial arts is not an end goal. It is more like reaching the starting line of the journey. At the higher levels, this learning includes the willingness to embrace paradox in many ways.

Traditional karate training obviously places a big emphasis on learning the basics. The only way to do this is through repetition so that it becomes automatic.

But the ultimate goal is not to become a clone of others from the past. Instead, every single karate student has a unique signature style. If you try to develop your signature style at the white belt level, you’ll just be fooling yourself. The style develops naturally over time without any extra effort through the process of repetition.

Learning from other investors about venture investing is a great shortcut. After all, nobody has the time to invent it all from nothing. To this day, I’m still reading Fred Wilson and Brad Feld on a regular basis.

You should absolutely learn from what venture investors are sharing both in public content and in private meetings.

But a copy and paste approach is unlikely to be optimal. Every venture investor’s background is unique. Each era is different. And it’s all path dependent. As an example, one of the big differences about our team at Fresco Capital compared to most other venture investors is our global cross-border approach. Most early stage investors are local and that works for them. We’ve chosen to be different precisely because of our background and experiences.

Instead of a copy and past approach, better to take the time to find trusted partners and work together with them. Co-create solutions that meet your unique needs. The ideal partners adds strengths to fill your gaps. This could be knowledge, network or other resources.

A key part of our global approach is working with local partners who are on the ground everyday in the local market. So just being global is not enough — working with these local partners is a key differentiation.

Martial arts starts with physical training. At a certain point, however, the mental and spiritual aspects of martial arts become more important than the physical training.

This doesn’t mean that the physical training is not important. The physical training is a gateway to reach the mental and spiritual benefits. Rather than being independent, they are integrated.

Venture investing starts with financial returns. This has to be the foundation. And many people do view venture investing as a box that takes money in and spits money out a few years later.

But this view overlooks the potential direct and indirect benefits beyond just the box of cash perspective. There can be positive effects on revenues, efficiency, and speed for related businesses. There may be harder to measure, but perhaps even more important, soft benefits such as upgraded team skills, improved innovation and entirely new business units which grow larger than existing businesses. Most importantly of all, all of this investment in innovation can, and should, be used to actually improve people’s lives.

It’s important to emphasize that these additional benefits are unlikely to materialize if financial returns don’t set a strong foundation. So start with the financial returns. But don’t limit your imagination to a box of cash. The ultimate potential is much bigger.

Venture capital investors are always questioning and challenging assumptions in other industries. It’s important that venture capital itself faces the same kinds of questions and challenges.

While industry insiders are looking for new ways to differentiate, a little extra push from external forces can only help accelerate the process.

Ultimately, the best way to learn something is share it with others. In karate, this means training new students and then having them train students. This passes on the physical skills plus also the philosophy and values. None of this can be truly learned by reading a blog post or watching a video.

There is no substitute for person to person training.

Historically, venture capital was a very secretive industry. Knowledge was not shared and venture capital firms put a lot of efforts into controlling information flow. This started to change in the past 15 years as the industry started to open up. Blogs and in person events have allowed people to learn more about venture investing. But the reality is that most of the activity is still behind closed doors.

True innovation requires an open ecosystem, and venture capital also needs to join this trend. So our view is that successful venture investors should not be trying to hide the secrets of investing from others.

We believe there is tremendous value to be created in sharing knowledge about venture investing with others. More and more new investors are getting involved in venture capital. Without effective co-operation, that money may be completely wasted on bad investments.

Rather than hoping that other investors fail, we believe that the startup ecosystem desperately needs more high quality investors. This is not a zero sum game.

Of course, the challenge is to identify the right kinds of partners. There has to be an alignment of both values and incentives.

There’s a saying in karate: “a black belt is just a white belt who never gave up”. Learning to learn is the most important lesson of all. I’m still learning plenty about both karate and venture capital.

It’s this learning that is the secret power of how we can transform venture capital one person at a time.

Imagine a giant spaceship—a ship that’s large enough to carry every single human on planet Earth. Even though the construction is far from finished, the boarding has begun! With the children mostly seated and ready to go. With great excitement the Earth is enveloped with a buzz about the upcoming trip.

But something’s amiss. The spaceship is consuming billions of dollars and millions of man-hours each year, yet there’s a small group of people desperately trying to point out that the project has a problem. It’s missing a steering mechanism!

Naturally, they are not heard because of all the noise of the construction. Engineers point out that working on the steering wheel of such a powerful spaceship is a complete waste of time.

There are numerous factions dismissing the group of—“too paranoid!”. Those factions can be roughly divided into 4:

1. This thing will never take off anyway, at least not in the next 300 years

2. Steering is trivial, with enough powerful engineers the spaceship will auto-steer itself

3. It’s pointless wasting precious resources on trying to control a spaceship this massive

4. It’s more important to get it off the ground, rather than worry about backward and selfish issues such as payload safety

Naturally with such a sensitive topic, many of the top engineers feel massive pressure to ignore this group of dissidents. Signalling sympathy with them may suggest that they are actually right. This may result in a diversion of funding and engineering hours from their part of the main engine!

Although contradicting in many ways, the factions have 2 things in common. 1) they are making excuses why nothing needs to change, and 2) they are trying to hide a grossly embarrassing blunder: the architects and engineers simply forgot to design for a steering mechanism.

This is a metaphor for Artificial Intelligence research, that Jaan Tallinn used at his talk. His story is a reflection of what the state of AI research and development was, only just a few years ago.

Jaan enthusiastically continues:

Metaphors are to be taken with a grain of salt, but this one is particularly interesting, particularly illuminating. Let me recount the similarities:

First: the moment when AI exceeds human level intelligence is often referred to as “takeoff” . People often debate whether the takeoff is going to be “hard” (in other words, too quick for society to react) or “soft”.

Second: the takeoff is going to affect everyone — but especially children, because they are “closer to the future”. The potential impact of AI takeoff is often compared to those of the agricultural and industrial revolutions. I’d go a step further, and analogize it to the invention of brains by evolution.

Third: getting a rocket to take off smoothly is hard. Designing a robust AI take off, is also hard . There are hard engineering problems, quoting AI-risk researcher Eliezer Yudkowsky: “Aligning superhuman AI is hard to solve for the same reason [as] a successful rocket launch is mostly about having the rocket not explode, rather than the hard part being assembling enough fuel.”.

Red eyes? Check. Big Bad Robot? Check. Worst that can happen? Think again

.Fourth, it looks likely — or at least plausible — that we’ll only get once chance to get this right. If the takeoff catches us unprepared, the result might be a disaster of cosmic proportions. Eliezer Yudkowsky again: “If you want a picture to symbolize what we’re worried about, don’t imagine a picture of a Terminator robot with glowing red eyes; imagine a picture of the Milky Way with a 30,000-light year-diameter sphere gapped out of it, centered on Earth’s former position.”. Yes, thats how large of a disaster this would be.

Fifth, for decades now, billions of dollars and man hours have been poured into creating ever more powerful metaphorical engines. To the point where AI is now smarter than humans in many domains. Yet the budget and talent that humanity has spent on the steering mechanism — that is, making AIs more predictable and controllable — can be rounded to zero. Humanity spends more on anti-tobacco advertising, than this.

Sixth, if you asked AI researchers just a few years ago about the control problem, you would have got all these conflicting answers — it felt like this line in a Dire Straits song: “two man say they’re jesus.. one of them must be wrong.”

Seventh, there was a lot of peer pressure to stay mum about the AI control issue. Although this has improved, unfortunately, it still exists. Attend a panel discussion on AI and you can observe the very real unease they experience sitting next to each other — it takes real effort to acknowledge the issue when their colleagues are around.

Anecdotally, two AI researchers walk into a panel discussion: Both very concerned about the AI control issue; both equally surprised to find each other at an AI risk conference. Prior to this “coming out of the closet” moment, the supervisor-student relationship they had spanned over 9 years.

If you are still unsure of the magnitude of the task at hand, allow me to quote a few notables:

“Let us now assume, for the sake of argument, that these machines are a genuine possibility, and look at the consequences of constructing them /…/ it seems probable that once the machine thinking method had started, it would not take long to outstrip our feeble powers/…/At some stage, therefore, we should have to expect the machines to take control”.

–Alan Turing, widely considered father of computer science said this over 65 years ago.

Here’s one:

“If we use, to achieve our purposes, a mechanical agency with whose operation we cannot interfere once we have started it, because the action is so fast and irrevocable that we have not the data to intervene before the action is complete, then we had better be quite sure that the purpose put into the machine is the purpose which we really desire and not merely a colorful imitation of it.”

In conclusion, indeed the entire field simply forgot. But it’s not all doom and gloom. Having painted such a depressing picture, let me change my paint colors for some of the most recent positive developments.

At the start of 2017, people are planning for the year, quarter, month, week and even day. If you plan for 10 years, that’s viewed as long-term. A few crazy people have a 100 year plan. But who has a 1,000 year plan?

Hiroshi Tsukakoshi. I came across his masterpiece, Tree-Ring Management, at a bookstore in Narita airport, hidden in the tiny English section between travel and language books.

Tsukakoshi gives a 100 year calendar to all of his new employees when they first join and also asks them to think about their 1,000 year plan.

Why?

He gives his own reasons in the book and you should read those directly from him. Here’s why I like the idea.

1) Take the long view, appreciate now

It’s not about me or you. It’s not even about my children or your children. It’s about generations upon generations in the future. That gives us perspective from the long view. To see beyond the horizon.

At the same time, the length of our individual lives is insignificant. Mark your forecast death date on a 1,000 year calendar. Even if you’re off by 23 years, it’s still roughly in the same spot. This gives you the emotional conviction that time is short. Appreciate the moment you have right now.

2) Dream big, start small

To make a positive impact that lasts 1,000 years ain’t easy. It’s like rolling a snowball down a hill. Even when you die, the snowball is going to be small. But if the snowball is made in the right way and the hill is long enough and various random elements align, just maybe it’s possible that in 1,000 years the snowball is still rolling and growing. The only way to get there is to dream big.

To make that giant snowball, you don’t start by building a giant snowball. You start by making a small snowball. Then finding a mountain. Then rolling. And learning from what happens. Maybe you made a mistake creating the snowball. Maybe it was the wrong timing. Maybe it was the wrong mountain. Keep learning and doing. But start small.

3) Everything connects, improve yourself

We’ve got social networks, airplane networks and AI networks. The list is endless. In the past, it really could take 1,000 years for an idea to spread across a network. Now it can take 1,000 milliseconds. This creates a giant opportunity for a 1,000 year plan to impact more things faster and is one key difference from the past.

But everything being connected is also overwhelming for us. A 1,000 year perspective helps eliminate the noise. Before I can tell you how to improve, I’d better start by improving myself. Before you tell others where to focus their attention, it’s worth managing your own attention habits. Before we can change history, we have to be able to change ourselves.

What?

If you take a 1,000 year view, what should you do?

1) Find something

Explore. Maybe you’ll find something new. And it’s not just about physically going somewhere. Zero, heliocentricity and gravity were all found.

2) Make something

Create. Maybe people will like it. The wheel, the Tao Te Ching and the Mona Lisa are still pretty popular.

3) Change something

Transform. Maybe there’s a better way. Politics, religion and business are all in desperate need of an upgrade.

How?

Some people are already working with a 1,000 year plan mentality.

But it can be hard to start. Here are a few ideas.

1) Ask

Take a look at something around you right now and ask “is this the catalyst for my 1,000 year plan?” Most likely the answer will be “no”. So keep looking, and asking, all day. By the end of day one, you should have at least 101 bad ideas. Keep going till you find something interesting.

2) Observe

The next time you feel happy/surprised/angry or maybe just have a funny feeling in your gut, think about what’s causing that. Triggers of emotions tend to be good places to start looking. But don’t stop with emotions. Start observing everything.

3) Remix

Take two random things and combine them. The new remix is probably a bad idea but save it just in case. Make 99. They’re all probably bad but save them just in case. Keep going and at some point you’ll start to notice patterns and outliers. Follow those.

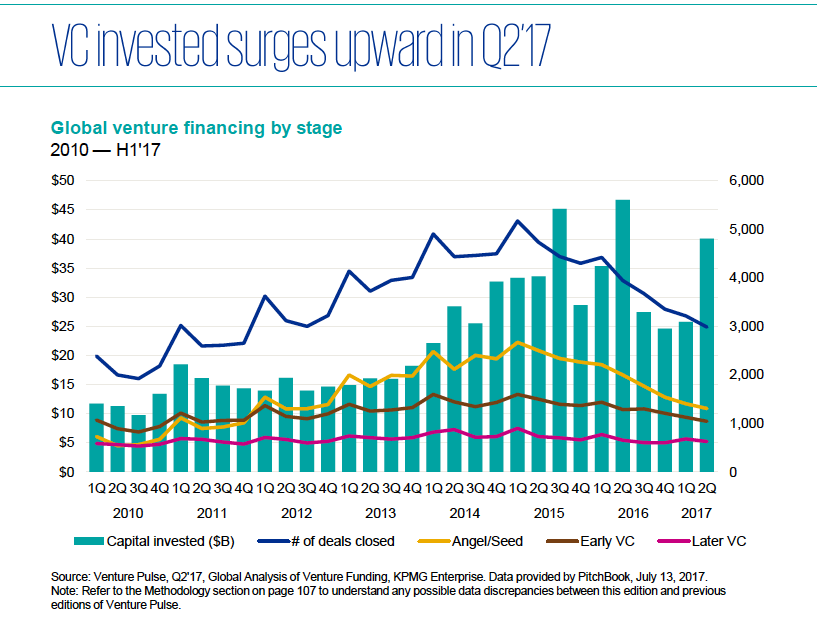

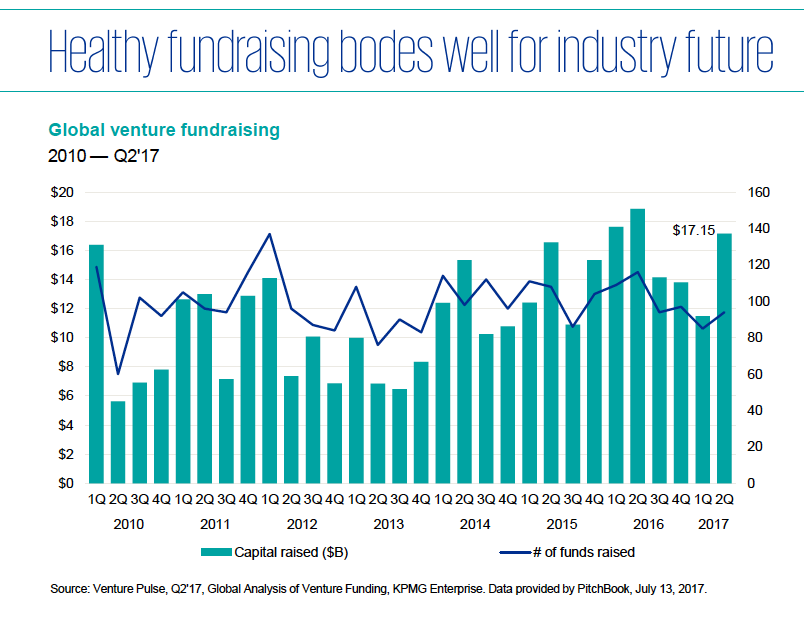

Headline numbers look good for global VC investment during the 2nd quarter of 2017 but the more interesting story is what’s going on underneath the surface.

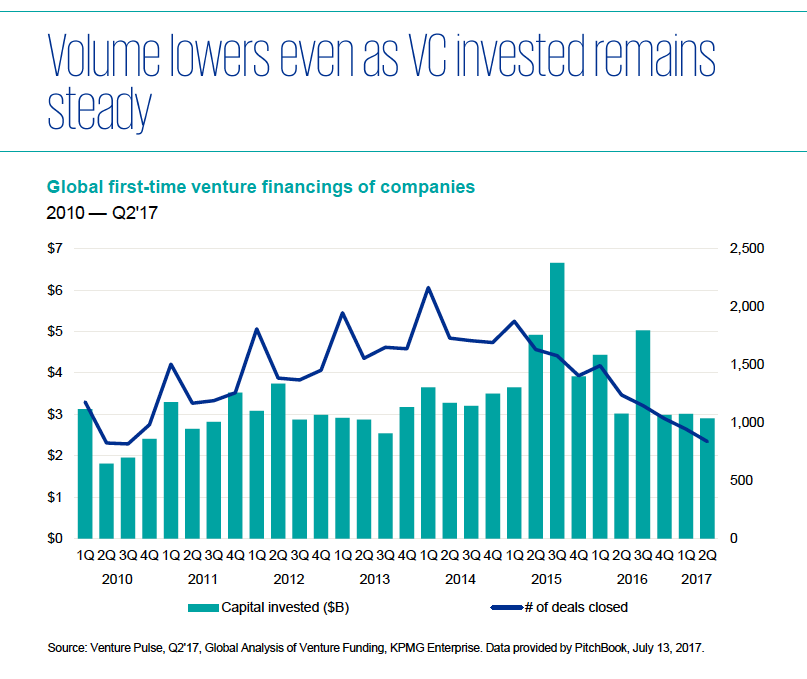

Digging into the details, below is the trend for first time investment activity (thanks KPMG + Pitchbook for crunching the numbers).

Even taking into account stealth rounds which have not been announced, the number of new companies has not been keeping up with the $ invested. And if you take the data at face value, the number of rounds is back to levels not seen in several years.

Instead, VC investors have been adding more to existing companies.

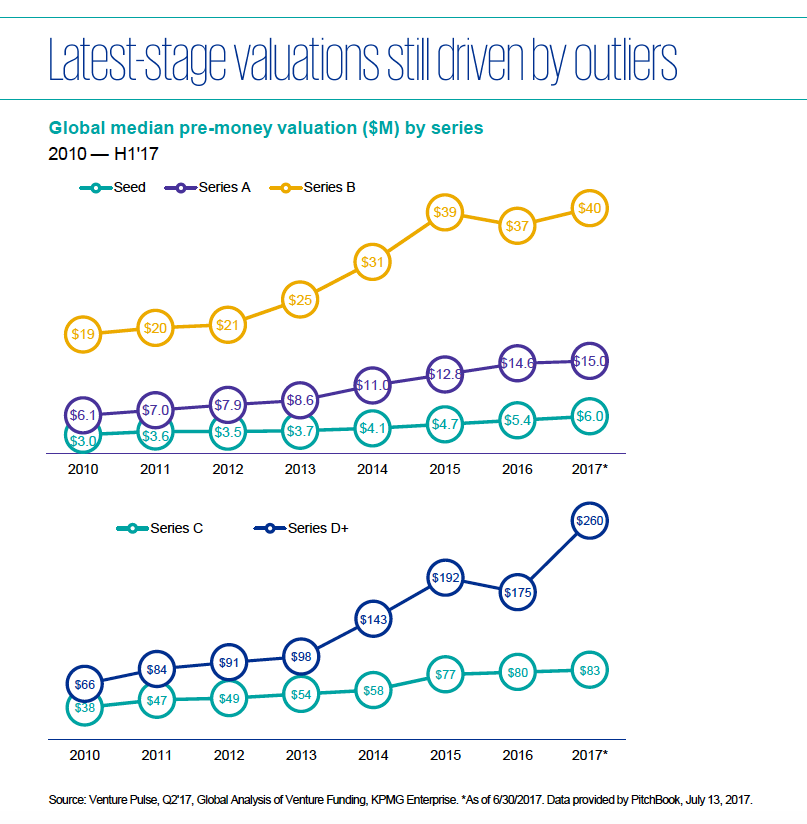

The increase in round size can be seen in most rounds, with the obvious outlier being the late stage Series D+. The above numbers are median, so the $40M figure likely understates the outliers.

The median pre-money valuations above tell a similar story:

fat rounds are back.

Why?

First, VC funds are cashed up.

VC funds are continuing to raise $ at an impressive rate. If you’re familiar with the timeline of how VC funds deploy capital, one guarantee is that managers will invest this money. They’re not going to give it back next year saying “I can’t find anything to do with it.” The capital will be around for, oh, about the next 10 years. VC funds will invest in something.

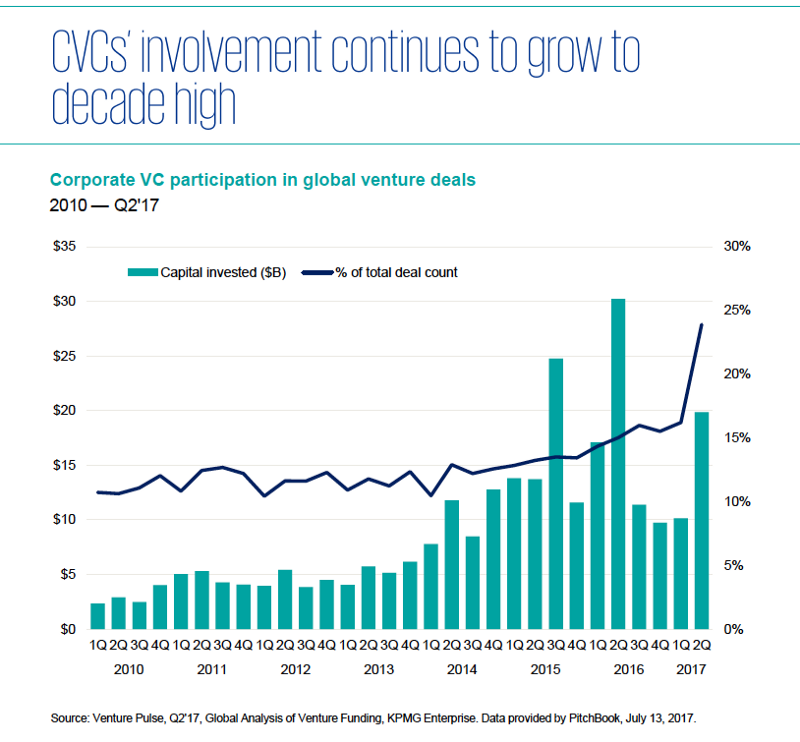

Second, corporate VC funds are having a big impact.

The rate of participation has been increasing steadily and in this last quarter they have been even more aggressive. Many of these funds are structured with external investors, including the headline grabbing Vision Fund. So like traditional VC funds, the capital should be around for several years (as contrasted with pure balance sheet investment from corporates which can be harder to predict over time).

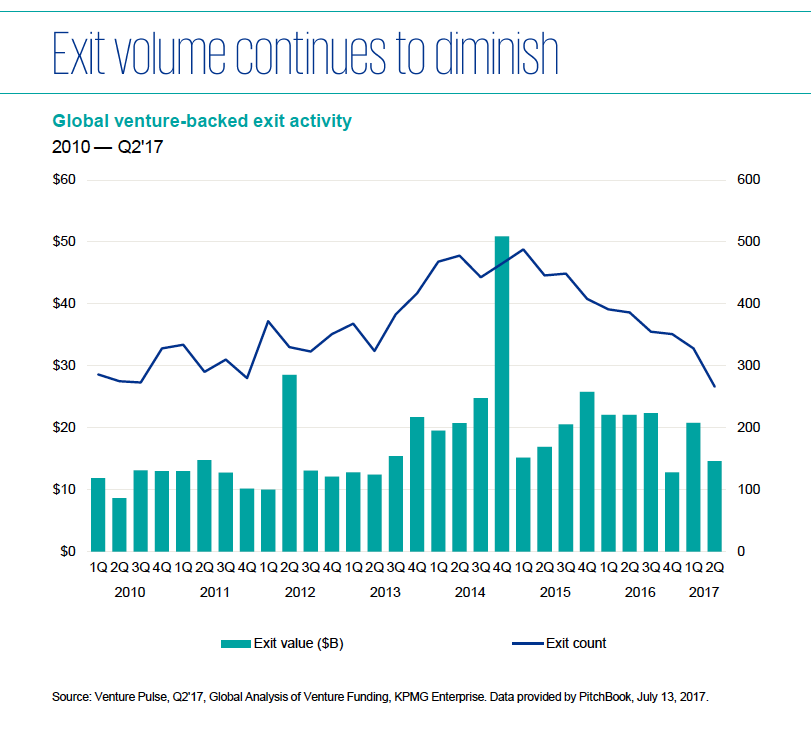

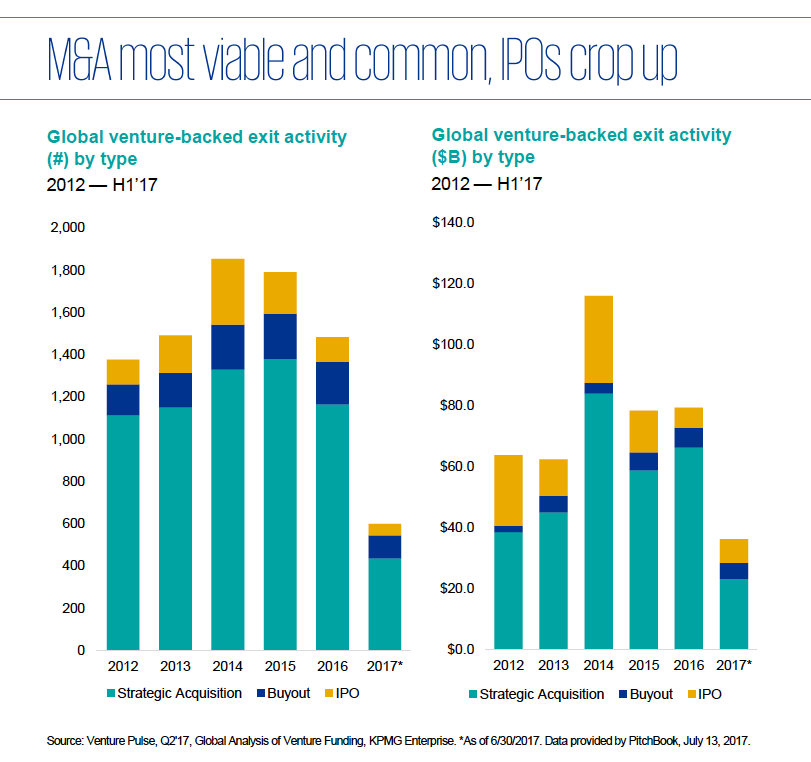

Third, exit trends have been lukewarm for VC backed startups.

This has meant that late stage companies are staying private for longer. Those fat rounds are in some sense becoming short-term substitutes for M&A and IPO exits.

So there’s an interesting paradox.

On the one hand, corporate VCs are more active than ever before and investing aggressively in late stage fat rounds.

On the other hand, corporate M&A activity is not keeping pace.

Based on the lifecycle of capital raised, expect VC funds to continue investing in existing companies.

However, if market sentiment deteriorates, fat startups will become the victims of cap table recaps. There will be money, yes, but the terms will be harsh.

For startups, VC investors, and LP investors in VC funds, now would be a good time to remember the benefits of capital efficiency. For startups especially, make sure you understand the terms of rounds, not just the headline valuation.

Fat startup rounds are back. Let’s make sure we’re building healthy businesses because it sucks to be a fat, dead startup.