Our firm name Fresco Capital is inspired by the timeless fresco paintings of masters like Leonardo da Vinci.

You may wonder “how can there be such a thing as Leonardo da Vinci venture capital and startup lessons?” as he lived hundreds of years before our modern startup ecosystem.

Yet Leonardo da Vinci left us a record of his observations and opinions in amazing notebooks. Many of his attitudes and habits are explored in How to Think Like Leonardo da Vinci. Here are five Leonardo da Vinci venture capital and startup lessons:

1. Curiosita: insatiably curious approach to life. Curiosity beats raw intellect for anything related to startups because you need to keep asking questions. Once you assume that you know all the answers, the company is probably going to fail. On a related note, it’s hard to be curious about something when purely motivated by money. It’s much easier when you are driven for the sake of learning and money is the by-product.

2. Dimonstratzione: commitment to test knowledge through experience. Learning through books and from others is helpful but there is no substitute for learning through experience. The scientific method of formulating a hypothesis and then testing it is extremely valuable during this process. Also, the experience of surviving and growing through the failures of experiential learning leaves scar tissue, which makes you stronger in the future. Of course, it doesn’t always feel good at the time.

3. Sfumato: willingness to embrace ambiguity, paradox, and uncertainty. Startups are defined by ambiguity, paradox and uncertainty. There is never enough data or evidence to make any important decision obviously clear except in hindsight. Every choice has both pros and cons. Most of the time, the only choice is to move ahead into the unknown while maintaining an open mind about feedback just in case you need to change course quickly.

4. Arte/Scienza: balance between science and art, logic and imagination. Some people get obsessed about the technology in startups. In the process they forget about people and emotions. True success requires a blend of science and art, and this is especially true in the early stages of building a company. To build something with global scale, a basic human emotion needs to be satisfied at some point in the value chain, even if it can be described by cold, hard logic.

5. Connessione: recognition and appreciation for the connectedness of all things and phenomena. Nothing exists in isolation. Decisions, actions and results always have context. Startups by definition have limited resources and so it is especially important for them to leverage the surrounding ecosystem and do more with less. As part of that, systems thinking has to include a strong appreciation of time, including when to move quickly and when to be patient.

There are many modern theories about venture capital and startups but the reality is that the core principles for success have been around for centuries. These Leonardo da Vinci venture capital and startups lessons illustrate that he would fit right into the current global startup ecosystem.

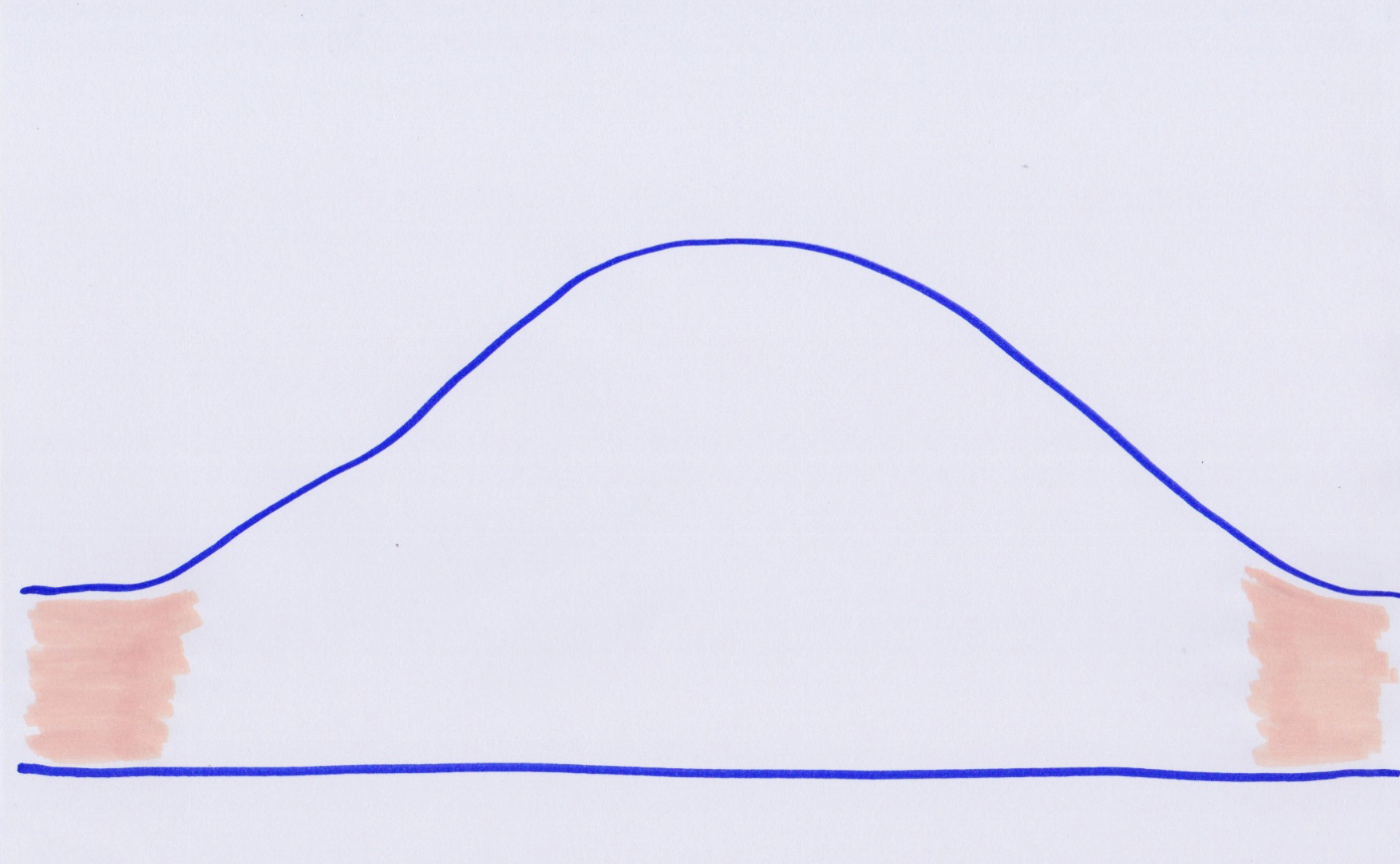

As venture capital investors, we are constantly looking for positive fat tails, companies that have the potential to generate extreme positive outcomes.

At the same time, not all fat tails are positive. There are negative fat tails. And as we look towards 2016 and beyond, it’s important to think about the risks. While there are many potential risks to consider, the following list of five fat tails focuses just on finance and economics because I don’t have the time to write a book this month.

To be clear, these are not predictions. In fact, the world may be better off if none of the following fat tails happen in 2016. But at least we should be prepared and resilient, just in case.

1. US dollar squeezes dramatically higher

If the US dollar rises steadily, that would not be a fat tail. But if it rallies sharply higher, that would fall into the category of fat tails. Why would that be negative? Historically, a strong US dollar is associated with tighter liquidity conditions globally. And so if we see a sharply stronger US dollar, that will be a clear warning sign of potential risks ahead. Currencies are typically the first financial markets to move. They lead bond markets, equity markets and private markets. As an early warning indicator, keep an eye on the US dollar. If it squeezes higher, get ready for more fat tails.

2. Unexpected rise in interest rates

The last interest rate increase by the Fed was in the summer of 2006. At that time, Facebook was only open to students, the iPhone had not launched and Tesla was an early stage startup. An entire generation of young people has grown up without understanding what happens when interest rates rise. An entire generation of old people has forgotten what happens when interest rates rise. It’s highly possible that we’ll finally find out in 2016. Historically, rising interest rates could not be called a fat tail event because this was a normal cyclical process. But if there is an unexpected rise in interest rates during 2016, it is best to approach this as a fat tail event because we really cannot predict how the results will play out.

3. Unicorn contagion

In every cycle, certain ideas capture the essence in a single word. In the current cycle, Aileen Lee’s concept of unicorns is that word. Now that some of these companies have started to show signs of being less than perfect, their connection as unicorns creates the risk of contagion within the group. More broadly, it’s still unclear what weakness within the group would mean for the broader startup and financial ecosystem. Perhaps nothing. Perhaps they are a leading indicator. At the very least, it’s worth keeping an eye on sentiment around unicorns.

4. Crowdfunding backlash

Crowdfunding is a transformational and positive idea overall. Like any transformational idea, markets have a habit of taking things too far. We’re now seeing new crowdfunding sites pop up weekly and some of the players are using very aggressive marketing tactics. There will inevitably be fraud, so the only question is the magnitude and the level of backlash. The fat tail event would be a larger than expected level of fraud, which would then lead to a strong backlash. This could impact both crowdfunding itself and also fintech generally. Compliance is already one of the fastest growing job in the finance sector. Unfortunately, a fat tail event in crowdfunding could accelerate this trend.

5. The Euro breaks up

Politically, it seems unthinkable. To be clear, this is not expected to happen in 2016, but it needs to be considered as a fat tail risk. If the Euro were to break up in some fashion, that would be the unwinding of a trend not simply going to the start of the Euro itself, but many decades earlier. The impact would be felt by everyone and while financial markets would take a back seat to the social issues, there would clearly be a massive impact on financial markets as part of the process.

The paradoxes of fat tails

Fat tails are full of paradoxes. The good news is that, individually, each of these events are unlikely to happen in 2016. The bad new is that fat tails are not independent. A stronger US dollar may actually happen along with an unexpected rise in interest rates and this in turn could trigger a unicorn contagion, a crowdfunding backlash and even a Euro break-up. And so, rather than thinking about them as five separate fat tails, we need to be aware of the possibility that they could cascade into one giant fat tail.

Fat tail events are almost impossible to predict. The only consistent prediction is if you can stay resilient during negative fat tail events, you’ll be around to take advantage of the remaining positive fat tail opportunities.

I recently recommended a friend for a PM job at a hot Silicon Valley startup run by another friend. The startup recently raised a big Series A and was looking to scale. I know the risk of linking up two friends in an employment scenario, however, my friend was more than qualified for this job and my founder friend really needed the position filled.

While my friend was more than qualified, interviewed well, and the team loved him, etc, the founder decided to pass on my friend. The reason: another candidate with the same skills and experience came along that they hired. The difference between the hired candidate and my friend? The candidate that was hired had the same PM experience but all at big companies like Facebook, Amazon, and Google. My friend has spend his entire career at startups.

My question is: was this the right move? If you had the choice between nearly two identical candidates and one had all their experience at big successful companies and one had their experience at successful startups, isn’t it safe to choose the candidate that worked at the bigger companies?

Put yourself in the founder’s shoes. You just raised a big Series A. You are being pressured by your investors to “go big or go home.” You have aspirations to be a big company. This is Silicon Valley, shouldn’t you hire the absolute best talent we can find? Shouldn’t you hire people who worked at Facebook and Amazon since you want your company to be big like them one day?

PMs that only worked at companies such as Facebook and Amazon are super qualified PMs. Huge plus. They also know next to nothing about building a startup. Huge negative. People from larger companies bring the bigger company process, procedure, and culture with them. This leads to premature scaling of your business. The problem is that your startup is not a smaller version of a bigger company. As Steve Blank says, a startup is an experiment looking for a business model, not a smaller version of a larger company. Facebook as over 10,000 employees and billions in profits. My friend’s company has less than 15 employees and no profits. Hire people comfortable working in that environment, who know how to bring a company from 15 people to 150 people. When your startup has 1000 employees and is super profitable you should start to hire PMs from Facebook. In between, you have to hire people who can not only do the job, but also help you grow the business, shape the culture, and constantly evolve the process.

I made this mistake several times at my past startups. At one startup we realized that we needed an HR manager. Since we had plans to “go big” we wanted to hire an HR manager who came from a big company. Big mistake. We were a team of 12 but all of a sudden we were doing 360 reviews and had to fill out a form in order to take a day off. At another startup we wanted to enter the “enterprise” space, so we hired some “enterprise” software people from a large enterprise software company and gave them fancy titles. The problem is that people who work as executives at big companies usually don’t roll up their sleeves and build a product. Nor do they know how to scale a company, they know how to keep a big company big, but don’t know how to build a big company. In addition they wanted to fly business class and have personal assistants, things that did not jive with our startup culture.

Avoid premature scaling at your company and hire not only the candidates with the best skill set, but also with experience in working at and building a startup. Later on when you are bigger and more mature should you hire the people with bigger company experience.

What are the secrets to a venture capital career path? Some people think operating experience. Others believe it’s all about the right connections.

My path to venture capital started as a waiter.

It was my second year of university and the lessons learned from having worked as a waiter have been surprisingly relevant to venture capital. To me, these lessons are the real secrets to becoming a VC.

Great service never goes out of style In any business, service is important, but especially where the business itself is a service. A waiter and a VC are both ultimately supporting someone else who is the primary decision maker. In the case of a waiter, it’s the customers sitting at the table. In the case of venture capital, it’s the founders building the companies.

But it doesn’t end there. As a waiter, you have to work with bussers, kitchen staff and other servers. As a VC, you must build strong relationships with dealflow sources, limited partners and co-investors. That doesn’t mean you have to be a pushover to everyone. Of course you have to stand your ground for important principles. But it does mean that you should think about the service you provide to everyone. Create value for others and you get more in return.

Know your customers and customize The best business relationships transcend the first transaction. For a waiter, that means repeat customers who return and ask for you by name. To build that relationship, you have to go beyond the basics and get to know their individual food preferences. You need to know the who loves extra cheese and who has a dairy allergy.

In venture capital, putting entrepreneurs through a factory style assembly line process is not the answer. Every company is different and, more importantly, every founder is unique. You have to go beyond standard founder/investor sound bytes to truly understand individual motivations. You need to know who loves aggressive debate and who prefers open ended questions.

Be a T-shaped person As a waiter, of course you have to understand your restaurant and the food it serves. That’s your area of expertise. But to be truly successful, you need to know a little bit about everything. Sometimes that means being a tour guide to visitors. Sometimes that means being entertainer to large groups. Sometimes that means simply being a good listener who asks thoughtful questions. Fortunately, these are all skills which are generally useful and not specific to being a waiter.

There is a similar situation in venture capital. The basic area of expertise is understanding the unique dynamics of venture investment and returns. But to be truly successful, that’s not enough. You need to understand technology and the impact it has on people. You need to be able to discuss legal issues in depth with lawyers. You need to have the soft skills to find the best teams and deal with a wide range of personalities. A T-shaped person has both depth and breadth.

Align incentives for performance Intrinsic motivation is ultimately the key to sustained long-term performance in anything. But incentives help. For many waiters, tips from customers can make more than 50% of total compensation. This additional upside beyond the base aligns incentives for better service for customers.

In venture capital, the numbers are bigger but the basic concept is the same. The classic VC structure means management fees as the base and performance fees as the true upside. If the fund size and management fees are excessively large, that is precisely when investors in the fund start to wonder if incentives are truly aligned.

Find gaps in the market There is no shortage of restaurants in the world and people who think they can serve food. Yet some restaurants remain empty while a few have lines around the block. The difference is that the successful ones have filled a real gap in the market. Filling a gap may be as simple as emphasizing family friendly service to attract children, who then bring their parents along. Or maybe you prefer to focus on serving the best tempura in your city. Find the gap and fill the market demand.

There is no shortage of money in the world. At its core, venture capital is a service of pooling and allocating money, so the only way to stand out is do something different. It may be as simple as focusing on companies in a specific city, like startups based in Vancouver. Or it may be as ambitious as building the bridge between startup ecoystems globally. Find the gaps and you will find the opportunities.

The road to a venture capital career Venture capital is fundamentally a service industry. Although there is no conventional career highway to venture capital, there are many unconventional ones. If you want to learn about venture capital, a good place to start is working anywhere in the service industry.

Forget the rigid highway, follow the winding pathway.

If Einstein were alive today, what would he think of our investment markets? He is vaguely attributed to have said that compound interest is the “most powerful force in the universe” but the evidence supporting this attribution is weak.

However, he would surely find it curious that we now live in a world of negative interest rates, where more than US$2 trillion has been invested in negative bond yields and banks are charging interest rates on deposits. Although the word deflation is constantly used in the media, the reality is still inflation, so whether measured in nominal terms or real terms there is no doubt that we live in a time where a certain group of borrowers are able to get paid to borrow money.

Since the driver of these interest rates is the cost of time, the financial sector has accidentally created a way for money to reverse the effects of time.

Besides being surreal, why is this important?

The obvious answer is that no serious investor should want to invest their assets into negative return assets if there are better alternatives. It is both a pessimistic view of the world and an inefficient use of assets.

Large companies are also taking a cautious view of the world, preferring to spend on share buybacks rather than new investment, with a record US$900 billion spent on buybacks and dividends in the US alone in 2014. In this case, share buybacks create the illusion of growth by shrinking the denominator, the number of shares outstanding. At an individual firm level, this can sometimes be the right strategy but can society overall shrink its way to prosperity?

For context, it helps to look at the size of investment at the opposite end of the investment spectrum, early stage companies focused on growth. Overall venture capital investment in the US was a record US$48 billion in 2014 and a closer inspection of the data shows that early stage deals received US$1.3 billion.

In today’s world, when the opportunities to create value through innovation are more exciting than anytime in history, society is investing the largest amount of money in the most pessimistic assets with the lowest expected returns and investing the least amount of money in the assets with the largest potential to create new innovation and highest potential returns. These are symptoms of a deeper problem: failure of the imagination.

As an early stage venture investment fund, this actually works better for us because it means less competition. Ultimately, however, early stage investment is not a zero sum game and so we would rather have more people invest to create more overall value.

Finally, if the perception is that there are no assets that can generate meaningful returns given the risk, investors are better off giving their money away because there is no shortage of social issues which have not been solved by markets.

Circling back to Einstein, some people may argue that he would be in favour of the current asset allocation by society because it appears to be made by rational decision making in a scientific manner. But his comments suggest otherwise. In Einstein’s own words, “imagination is more important than knowledge.”

Being an early stage investor is now a status symbol. For individuals, funds and companies. Unfortunately, not everyone should be an early stage investor focused on the seed stage. What are the key considerations?

How much time do you really have? This is the first question for everyone, from small angel investors all the way up to large corporates. No matter how much money you have, your main constraint is actually time. The most common feedback from people who have just started to invest in early stage companies is that the time commitment was beyond their expectations.

Every single investment made takes significant time, both in terms of due diligence before the investment and, more importantly, support after the investment. To build up a successful early stage portfolio, diversification helps because of power laws and so at least 15 investments but probably closer to 30 is the right size. In addition, to even find a single investment, most investors should first look at 100 potential companies. When you multiply the time commitment through that funnel, it suddenly starts to look like a full time job for one or more people.

Where is your geography? The traditional approach to geography in early stage investing is hyperlocal. The upside of this philosophy is the close contact with the founding team. The downside of this philosophy is that your universe of opportunities has been reduced significantly and you probably lose the broader perspective of what is happening in other markets. In today’s world, not having a global perspective is a competitive disadvantage.

Some investors, including ourselves, take a cross-border approach. While this provides a significantly larger universe of opportunities and a more diverse perspective, it is extremely difficult for most people to execute in practice. You need a team that is comfortable across both physical distance and cultural nuance. Most early stage investors are actually better off partnering with someone who knows how to do this rather than trying to replicate this skill set in house because it is not easy.

Who is your network? Clearly the quality of your network will be a key driver of both your investment opportunities and the value you can provide after investment. In the past, having a network of strong connections to people in high places was the ideal. Access by itself was a key asset. As the cost of building an early stage startup has collapsed, the doors for everyone else have opened up. Knowing people in power will always be valuable, but it is not the most important feature of a network anymore.

Instead, the ideal network is diverse and connects small worlds with loose ties. This means spending time with different kinds of people across demographics and skill sets. Unfortunately, most investors are simply not experienced with diversity. If you do not have a diverse network, find someone who does and partner with them.

What is your value add beyond money? Ultimately, money by itself is a commodity. At the early stage especially, where the capital requirements are smaller, having more money is not by itself a competitive advantage. In fact, the pressure of having large amounts of money to invest is actually counterproductive at the early stage.

Therefore, all early stage investors need to bring additional value beyond money. As discussed above, network diversity is a key point of differentiation. Domain expertise is another helpful factor and is fantastic when it works well. The challenge with domain expertise is ensuring that the investor is not trying to be an operator and run the business for the entrepreneur. It is important to ensure that investors understand the reality of what hands-on vs. hands-off really means. Ultimately, most investor value add is useful when it is complementary to the skills of the founding team, filling a gap. By definition, this is unique for each company.

Why are you investing? If your motivation is to find a status hobby, you will be in for an expensive lesson. When it comes to hobbies, collecting classic cars would be cheaper and cooler. While this goes for individuals, the same logic applies for more sophisticated investors. Family offices who want to dabble in angel investing because of the fun factor may be attracted by the hype but ultimately will find it both less profitable and less enjoyable than expected. Even corporate investors, who have jumped in aggressively into venture capital, need to have a clear strategy. In all the cases, from individual angels through to the largest companies, it is important to have a deeper motivation than simply because of the excitement.

Some people invest simply to learn while of course many also want to make money. In both cases, you may actually be better off by investing in a fund or syndicate because having a more experienced investor will most likely result in stronger learning and higher returns as compared to simply making your own basic mistakes. The data shows that early stage investors fall into two categories: those who know what they are doing and those who don’t.

There is no question that we need more early stage investors. But before jumping in, ask yourself the above questions. If the answers still convince you to jump in, then go for it. If the answers create some hesitation, then find more experienced investors and partner with them so that you can still get the benefits without creating new headaches for yourself.

Everyone is talking about replicating and building the “next Silicon Valley” with the rise of Silicon “roundabouts” and Silicon “beaches” in several locations around the world. While this is going on very few people are talking about how Silicon Valley is evolving: specifically that Sand Hill Road is now the Wall Street of the West Coast.

The rise of the “Uber” Round

More and more tech startups are raising hundreds of millions or even billions of dollars in later stage “uber” rounds. (I call these the “uber” rounds as a play on the German for “super” or after the company Uber that has raised well over $4 billion in Venture Capital.) As of this writing, Lyft has just closed a $680 Series E. According to Crunchbase, Lyft is one of 20 startups that have raised $1B or more in venture funding in the past 5 years.

Companies are going public later and later, a trend started by Facebook; instead of rushing to an IPO, companies are staying private longer and are taking more and more uber rounds. (Some people think that these companies should be going public as the investing public can’t participate in the later stage growth, allowing the rich to get richer.) The average amount of money that companies have raised before going public has been going up, more than double since the 2008 downturn.

What is Going On?

Most pundits think that companies are staying private longer to avoid the hassle and expense of going public as well as regulations like Sarbanes-Oxley. While those are all reasons to stay private, the real reason is that Silicon Valley VCs on Sand Hill Road have evolved to grow larger and focus on late stage massive growth.

Typically an IPO is for massive growth. A company will get to a certain stage of maturity and then raise anywhere from $300m to over a $100b at an IPO. The IPO accomplishes a few things: allows early investors and employees to “cash out” and sell their shares to the public as well as provide much needed capital for massive growth.

Today companies are delaying the IPO and raising the growth capital with their uber rounds. On the surface this looks crazy. But in reality, it is genius.

Lean Startup and Uber Rounds

Let’s take a made up startup LeanCo as an example. Assume LeanCo already took a Series A ($8m) and Series B ($30m). Now they are kicking butt and are growing at the same rate as the other high performing startups. Say they have well over $250m in sales, expanding market share, healthy margins, and are expanding internationally. This is the textbook case for an IPO.

What would happen is that LeanCo would go to a big Wall Street bank and raise approximately $5-$10+ billion in an IPO. After all the costs and fees and the Wall Street bank’s cut, the company would have a lump sum of money, let’s just say $5b. Now the company has the war chest it needs in order to grow. Typically LeanCo will acquire smaller rivals, enter new markets, and build out new products and services.

Instead, the LeanCos are choosing to raise billions for growth before an IPO. Instead of raising $5b in an early IPO, they are raising $2-5b privately before a much later IPO (at a much higher valuation.) They are raising the money $400 or more at a time. Here lies the genius of this approach: LeanCo only raises what it needs, when it needs it in a private (closed) market that will provide a higher valuation than a public one. There are also other benefits to staying private during the growth stage, like not disclosing your financial health and spending to competitors.

For the investors, this is actually a much more conservative approach. By only giving LeanCo the money when it is needed and doing it incrementally, LeanCo has to operate in iterative cycles similar to the Lean Startup and Agile Development. For example, if investors provided LeanCo with $5b in one lump sum, LeanCo may spend it unwisely feeling that they have a lot of capital on hand. If investors give LeanCo $400m or so at a time, LeanCo will have to take an incremental approach. If LeanCo were to go under after an IPO, investors would lose all of the $5b. If LeanCo were to fail after raising “only” $2b, investors lose far less money.

The Post-IPO World

The VCs on Sand Hill Road in Menlo Park have changed the game. I remember in the .com bubble, the largest Venture Fund was $1b and the largest deal was around $75m. Now the VC funds on Sand Hill Road are all well over a few billon each and think nothing of leading a $500m round.

Eventually the startup companies are going public, however, that is only because at some point they have to in order for the VC investors to sell their positions and the employees to cash in their stock options. I’m sure that over time, Sand Hill Road will evolve past the IPO, where companies stay private forever and large East Coast financial institutions buy back those positions from the VCs and earn returns via dividends, etc. You are already starting to see the signs of this when large pension and investment banks such as Fidelity, T. Rowe Price, and Goldman Sachs are part of the last round of financing for companies like Lyft, Box, and Uber. In the future, you won’t be able to buy shares in a Facebook individually, but you will buy shares in a Fidelity “Silicon Valley” Mutual Fund. Silicon Valley is disrupting Wall Street.

What Does this Mean for Startups in Silicon Valley

We all know that New York City and Wall Street is the IPO center of the world. Did a startup have a competitive advantage by being located in New York? As a native New Yorker who built three startups in New York City, I can confidently say no. Mark Zuckerberg proved that when he showed up to his Wall Street pre-IPO meetings in his hoodie. When your company is ready and has the right numbers, the Wall Street Investment Banks will work with you, no matter where you are.

What about tech startups located in Menlo Park, Palo Alto, or Mountain View, close to Sand Hill Road? (Sticking to the geographical description of Silicon Valley.) Same thing, when your company is large enough to take the uber rounds, it does’t matter if you live in Menlo Park or Montana, or Mongolia, the VCs on Sand Hill Road in Menlo Park will work with you. You are already seeing this with startups being located in the City of San Francisco and not down south in Silicon Valley. The larger established companies such as Facebook (Menlo Park), Tesla (Palo Alto), Google (Mountain View), etc are down in Silicon Valley, but the young, early stage startups are up in San Francisco. This means San Fransisco is about the startups and Silicon Valley is about the money.

San Francisco is the new Silicon Valley. Silicon Valley is the new Wall Street.

I’m super lucky to be from New York City and have lived in both Europe and Asia before settling down in Silicon Valley two years ago. I’ve also been lucky to work at a startup in Eastern Europe that grew to be so successful that many of my former co-workers there have become either Angel investors in the region or left to do their own startups. Of course, Fresco Capital is geographically diverse with 2/3 of the partners overseas. Because of this I get to meet a large amount of startups from outside of Silicon Valley, particularly from overseas.

Typically when they come to Silicon Valley for the first time, I am their first visit. (Honored!) That said, they all ask me the exact same question: “Steve, we are about to raise our Seed round of $1m, can you introduce us to some investors that will put our round together?”

This is when I have to give the founder “The Talk.”

The Talk(TM)

I say that raising a $1m Seed round in Silicon Valley is easy, just go to a Starbucks in Palo Alto and trip a few people and when they fall down, $100k will fall out of their hoodie. Aim for someone with a Facebook or Google hoodie and maybe $200k will fall out. While this is a (slight) exaggeration, the point is that most seed rounds that are not lead by an institutional investor are pieced together by wealthy Angel investors usually $200K or so at a time. While a foreign startup has the potential to meet Silicon Valley Angel investors on a two week visit, typically, you raise this money via a personal network. (Your’s or your advisor’s.) If you are not from the Valley, you won’t have this network and would need to stay and network for months and months, burning cash and wasting time (that should be used to build your startup).

I Know Nobody in the Valley, What Should I Do?

I always suggest to non-local entrepreneurs to go raise their seed round locally in their home market where they have a network of potential investors. It will be easier and faster than trying to raise money in the Valley where you don’t know anyone. You can then come to the Valley for your Series A from a position of strenght after you have nailed your business model.

This presents a problem insofar of the level of sophistication of the investors in your home market. While I agree that most markets are not nearly as sophisticated as Silicon Valley, there are “Valley” type investors in all markets these days, you just have to go find them. The easiest way: build an awesome business. I was talking with by buddy Pascal the other day about valuations in Europe compared to the Valley. Startups outside of the Valley tend to have less of the valuation inflation that the Valley startups do. If you build a sustainable, repeatable, scalable business with funding in your local market at a competitive valuation, when you come the Valley later on to raise a Series A, you will find it easy to raise money!

The question is usually presented as if it were binary and a constant state of being across companies and situations. But every company is unique and even the same company goes through a variety of different situations over time, requiring different levels of engagement from investors.

Investors who would like to be completely passive and simply invest money are better off investing through a fund, syndicate or angel group. Similarly, at the other extreme, people who would like to be involved with every single decision made by a company because of their operating expertise probably should be operators rather than investors.

That leaves a sizeable middle ground with a more interesting question: what factors should influence the level of investor engagement?

What are the consequences? Stating the obvious, there are typically key inflection points for every company. These can include decisions about team, fundraising, product, business model and external partnerships, so it is not necessarily in one specific category. Rather than trying to make decisions for founders, the best way investors can add value is to help teams reflect on their decision making process.

If the founders are choosing between business models, investors should be able to help. If the founders are choosing between business cards, just get it done.

What is the level of uncertainty? When a decision is important and also has a high level of uncertainty, investors can help teams to explore scenarios in more detail. This can include providing personal context, researching background information or identifying key assumptions. Once again, the emphasis is on process rather than conclusions.

When choosing to enter a foreign country, investors with cross-border experience can help reduce the uncertainty. Understanding the nuances of local culture is hard to do from media reports alone because the media focuses on the extraordinary rather than the ordinary.

When is the timing? Many of the most challenging decisions have important consequences, high levels of uncertainty and significant time pressure. In these cases, there is simply not enough time to do all the necessary research. Investors can add value by referencing rules of thumb that have worked in the past which may be relevant. These rules of thumb should be based on process, not the final answers. Just make sure that you have investors who respond quickly because no amount of experience can help if they don’t respond in time.

During last minute negotiations with strategic partners, it is easy to get caught up in the moment, especially with sleep deprivation. Experienced investors can help to decide the difference between tough negotiations and simply an unfair deal.

Does the investor bring something to the table? Important decisions are contextual. Investors with diverse experience have the ability to identify which experience is relevant and match for fit. Investors with recent domain expertise, regardless of diversity, can also help. Of course, if the investor experience is not relevant, then even giving input or advice may be counterproductive. So it is important for investors to have a high level of self-awareness about when they can truly add value.

Investors are typically self-confident and charismatic. But investors are also often wrong. When in doubt, founders are statistically correct to assume an investor is, on average, giving the wrong advice.

Who else can help? Successful founders have the ability to attract investors with complementary skills. In addition to self-awareness, investors should be able to consider the ability of other investors and partners to provide input and support. Having co-investors work as a team to support a company is more powerful than simply a random collection of individuals. Furthermore, investors with a high quality and diverse network can quickly find others to add additional support.

Investors sometimes like to use the coach metaphor with founders as the players. Flip that metaphor upside down and think of the founder as the coach and the investors as the players. Then assemble the best team of investors, not simply the best individuals.

Every company is unique and its needs change over time. Forget thinking about hands-on or hands-off investors because founders should not have to settle for either extreme. The answer to hands-on or hands-off is simple: yes.

In my role at Fresco Capital and as an advisor to several startups, I’ve seen it all with founders: disputes over shares, disputes over money, disputes over a new laptop, founders break up, a founder falling ill, founders get married, founders get divorced, founders get into physical arguments. Often this leads to one founder completely disengaged from the business and still holding a significant amount of equity or even a board seat. We’ve seen this at large companies such as Microsoft and more recently at ZipCar. Typically you need this equity to hire executives or attract investors. Worse, if the company is being acquired, you now have one founder who can hold up the deal if they are on the board and disengaged. That of course is a problem, but one that can be solved with a dynamic founder agreement.

Founder Troubles

Most founders settle the division of equity question with a static founders agreement. It usually goes something like this:

Founder 1: 50%, vested over 4 years, 1 year cliff

Founder 2: 50%, vested over 4 years, 1 year cliff

This solves a lot of problems, such as if a founder leaves after two years, they will still have 25% of the company but give up the second half of their equity. What happens if one founder is not “pulling their own weight” or contributing enough to earn the vesting (in the other founder’s eyes) but did not leave the company? What happens if they have to leave due to illness or personal emergency? What happens if there is misaligned expectations as what skills a founder brings and what role a founder will play?

I’ve seen this happen at one of my own startups. One of our founders was a lawyer and at the time we sold the company, he could not represent us due to it being a clear conflict of interest. While the legal fees were not all that bad (maybe $50k), to this day, almost ten years later, my other co-founders are still mad at the lawyer co-founder. This was clearly misaligned expectations.

This is what Norm Wasserman calls the Founder’s Dilemma, or the unexpected consequences of not spelling out the roles and expectations of the founders early on combined with the unintended complications of a founder leaving early or disengaging. He suggests a dynamic founders agreement.

The Dynamic Founders Agreement

The dynamic founders agreement is a way to mitigate the risk of an underperforming founder by changing the equity based on pre-set parameters. For example say I am starting a company with my friend Sam. Sam and I agree to a 50-50 split with Sam being the “business guy” and me being the “tech guy”. The assumption is that I will be the coder of V1 and lead the development team after we get funding. But what if I need to leave the company due to family emergency? What about if I decide that I don’t want to code anymore, before we can afford to hire a developer? What if I only give 30 hours a week and consult on the side?

A dynamic founders agreement is a big IF THEN ELSE statement that spells all of this out. IF Steve works as expected, his equity is 50%, if Steve has to leave the company, if he becomes disengaged, here is the pre-negotiated equity and if we have to buy Steve out, here are the terms. For example:

IF:

Steve works full time as CTO performing all the coding and technical duties of V1, his equity is 50%, vested over 4 years, 1 year cliff.

ELSEIF:

Steve works part time, is disengaged, or we need to hire developers sooner than expected, his vested equity is reduced by half and he forfeits his unvested equity. Loses board seat.

ENDIF:

If Steve has to leave the company because he needs a job or a family emergency: if Steve built V1 then the buyout is a one time payout of $50,000 USD cash or 2% vested equity, if Steve did not build V1, the buyout is 0.5% vested equity. Loses board seat.

Having a dynamic founders agreement won’t solve all of your problems, however, it will make the the process of removing a founder much less stressful. Sure some of the language in the dynamic founders agreement will be subject to interpretation, but the “spirit of the agreement” is much easier to follow or even if you have to litigate, more robust. If you never need to use the dynamic founders agreement, but built one anyway, it will force a frank and open conversation about roles and commitment among the founders. This only strengthens the relationship between founders, increasing the chances of success.