At the break, a group from Siberia approached me and asked if Fresco was really “open to anything”. Vasilii Efimov, representing Venture Company Yakutia, a Siberian VC, asked if Fresco would come and visit Siberia.

I was impressed with the region’s commitment to ecosystem development and the large group of diverse stakeholders assembled to make it happen; I committed to learning more and to visit Yakutia in 2018. The team at Fresco wanted to see how this model was working in a such a remote region and if we can learn from their efforts and help replicate it in other environments.

We talked about organizing a local Hackathon, similar to the Hackathon we helped organize in Pune, India. The goal of the Hackathon in Yakutia is to learn about the developer and tech ecosystem in Siberia and see how the Hackathon model brings ecosystem people together in remote regions. The Hackathon will be held later this month at the Higher School of Innovative Management which is a large professional development center.

Yakutsk, Russia

In addition to the Hackathon, we decided to organize a local startup mentor office hours and pitch event to give the local startups an opportunity to work with and pitch to an international group (besides me coming from Silicon Valley, I’m bringing partners from Hong Kong and Canada.) It will be a great learning opportunity for the local startups who don’t get a lot of international exposure. They will get some dedicated mentor time as well as have a group pitch event to gain feedback on their pitch as well as their business model. We at Fresco will learn more about Yakutia’s model of building ecosystems.

The team in Yakutia also organized an entire “IT Weekend” that consists of the Hackathon, the startup event, a few mini-conference sessions, local ecosystem tours, and visits to government, Techopark (IT park), university, and corporate partners.

Over the past year, we at Fresco Capital have had a lot of questions from our portfolio companies on Initial Coin Offerings (ICOs). Most of them were asking, “Should we consider doing an ICO?” Given the unforgiving volatility of cryptocurrencies, and the potential legal ramifications of an ICO (e.g. the US Securities and Exchange Commission (SEC) issued warnings on ICOs), we thought it would be a good idea to provide some guidance on the topic.

In addition to helping our existing portfolio companies navigate the choice to do an ICO or not, we have also been evaluating an influx of crypto-related dealflow (we passed on many, and have invested in one). Throughout that process, we learned firsthand that finding the right information to make a decision on an ICO is just as, if not more difficult, than actually doing one!

So, we decided to formalize our guidance in a document and distribute it to our entire portfolio, saving the portfolio companies weeks of research of their own. We have reached deep into our global network over the past year to get the best advice for our founders. The entire team at Fresco was involved in putting together a document, everyone from a super engaged intern in Hong Kong, to our Venture Partners, to all three of us General Partners. A few of our own investors or Limited Partners (LPs), have a lot of experience with ICOs, so they helped out as well.

The first version was sent to our portfolio companies, advisors, and some investors a few months ago. We’ve been told that most of our founders didn’t realize:

· ICOs take longer (4–6 months) and are more costly ($500k-$1m) than expected

· The classification of your token as either security or utility has massive legal, tax, regulatory, and economic consequences.

· The jurisdiction for your issuance is critical.

Since it was first published, some of our founders and investors have contributed back to the document, as well as asked if they can share it with their friends at other startups. Given it is such a quickly evolving market, we thought the best strategy would be to open source the document so that it can be a living, breathing, and evolving resource for the entire startup ecosystem.

The evolution of our brand reflects our evolution as a fund, a startup, and a platform.

When Fresco Capital first started investing in early 2012, one of the least impressive things about us was our website. To be blunt, it sucked. We know, because Tytus hand coded it himself in HTML. We also know because people told us.

However, as our entrepreneurial roots suggest, Fresco is not just a VC fund. We are a startup, too. And just like the companies we invest in, we are constantly evolving.

In 2017, we launched our third fund, we welcomed our 50th founder team to our portfolio, and we added our fifth Venture Partner to our growing network of local teams. We soon realized we had outgrown previous skin and it was time to embrace our own evolution; a time to refresh our brand, our website, and our messaging. So, we worked with one of our close partners, Rival Schools, to do just that. Given the team has world class expertise on localizing user experience, branding, and messaging to suit a global audience, we knew we were in safe hands.

We wanted a design that reflected our global team, our partnership based approach, as well as our belief that our team is greater as a whole than as a sum of its parts. We were aiming to visually represent the simplicity of our mission, but the complexity of our approach. Here is how we look now:

Our mission: Building global ecosystems

Although our shape may have a changed a little on the outside, Fresco remains the same on the inside. In fact, our growth has only strengthened our commitment and our excitement about our core mission:

You’ll notice our mission isn’t just about being the best at investing in technology companies. Just like our logo, the idea of “building global ecosystems” may seem simple, but it is an approach that embraces the complex.

An ecosystem can be defined as a complex network or interconnected system. Whether we’re working with founders, our LPs, or our partners, we believe the most effective investment strategy is to look beyond just us, and instead focus on empowering others. That is the only way to truly enable exponential change. One person, one product, one platform, one investor, one country, can only do so much. If we are able to build ecosystems filled with individuals, startups, and investors that are passionate about solving big problems, then the impact will be unimaginable in scale. And, if that’s not what we’re striving for, then why even be here?

Our approach: Thinking global, acting local

Our portfolio companies are leveraging technology to solve the world’s biggest problems in the future of work, education, and healthcare. These problems are global in scale, but implementing any solution requires a deep understanding and appreciation for local challenges.

It would be impossible for any one person to understand or appreciate the nuances of doing business in every local market, so we have focused on building a diverse team of specialists. Each with their own unique network, set of experiences, point of view, and passion. In our new website, we put a bigger spotlight on some of our favourite local partners, with whom we have worked with closely over the years and trust to be the absolute best at what they do.

Our motivation: Why we’re global

Though we are strongly motivated by our mission, we must also admit we’re not simply building global ecosystems out of the goodness of our hearts. There is a clear and direct connection between helping our portfolio companies scale globally and higher returns for our fund investors.

Global companies are worth more money — they have more revenue, less concentrated risk, and higher valuations. They can extend runway by optimizing their operations, increasing access to later stage capital, and diversifying their relationships with potential acquirers. We’ve seen this play out across our existing portfolio, which now spans 54 companies, 12 countries, 7 exits, and a total market value of US$1.6 billion.

We talk to and work with founders all day, every day, about how to build a company that scales and endures over time. Indeed, successful business models have mission, values, and financial incentives aligned by design. So it’s natural for us to apply the same approach in building our own business.

Our bottom line: We can’t do it alone

Given all of the chaos endured in the past year, we believe that now is the time to double down our mission. The world is faced with an unprecedented level of uncertainty, inequality, and risk, and it is our responsibility to work together globally to source, build, and scale the world’s most promising technology solutions to our most critical challenges in the future of work, education, and healthcare.

We look forward to hearing from you and working together toward as we grow and evolve as a firm, and as an ecosystem in and of ourselves.

For the last 200-plus years, capitalism has essentially been guided by one central tenet: delivering the most value to shareholders as possible.

Capitalism, of course, is not perfect.

So while companies scrambled to increase value for their shareholders, they did all sorts of atrocious things — forcing the government (or unions) to intervene on behalf of the citizenry.

In 1938, for example, the Fair Labor Standards Act became the law of the land, ostensibly outlawing child labor. In 1970, along came the Occupational Safety and Health Act (OSHA), which was designed to improve workplace conditions. The Family and Medical Leave Act became law in 1993, enabling workers to take extended breaks from their jobs for medical and family reasons without having to worry about becoming unemployed. There have also been laws passed to regulate the environment and prevent securities fraud.

The list goes on and on.

Focusing on the Wrong Thing

When companies are guided solely by maximizing shareholder value, management tends to focus on the wrong thing.

Capitalism, as it’s currently conceived, is far from perfect. Something needs to change — and everybody understands this.

This is why Bernie Sanders and Donald Trump — who actually had very similar messages — were so popular last election cycle. Both were a reaction to what is broken with the traditional model.

Capitalism is great — don’t get me wrong. But the misguidedness of focusing exclusively on maximizing shareholder value is what is broken.

Here’s where Bernie and others at war with capitalism get it wrong: Instead of focusing on the entire philosophy, they should be focusing on the shareholder value part of the equation.

Capitalism 2.0

I believe we’re in the middle of a defining moment. Capitalism is evolving into what I call Capitalism 2.0.

Capitalism 2.0 is straight up capitalism — but with a twist. Instead of focusing solely on shareholder value, companies operating under this model will prioritize the customer experience first and their contributions to society second.

By focusing on these two areas, shareholder value will automatically increase.

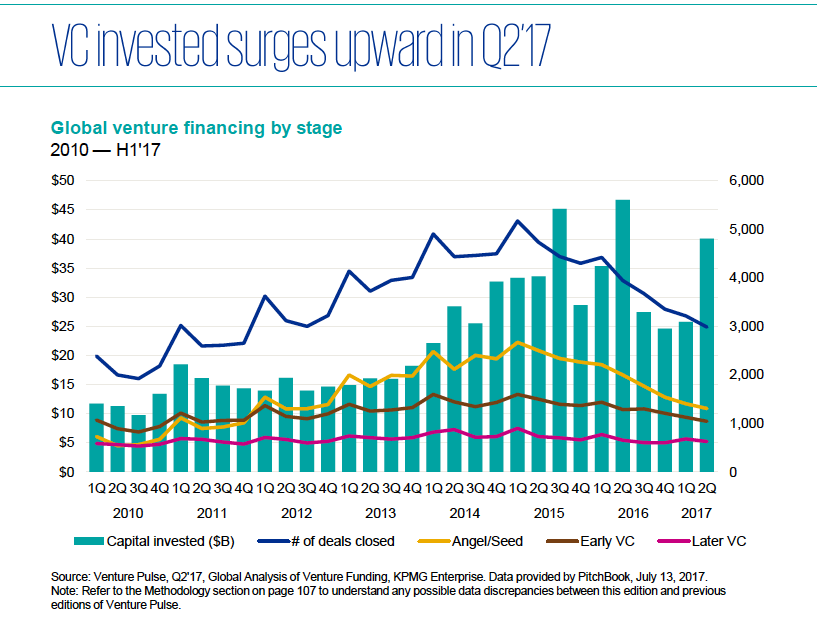

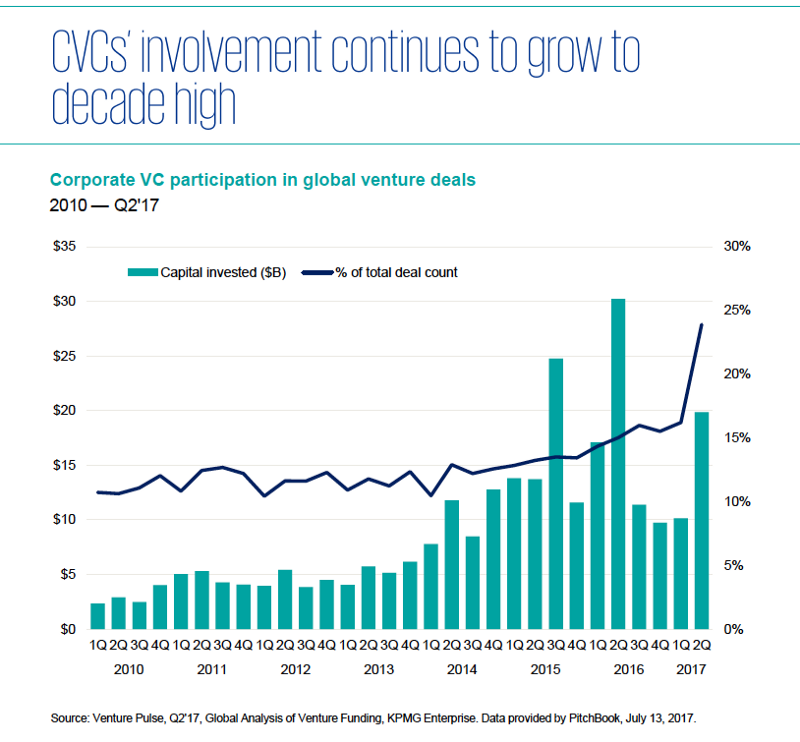

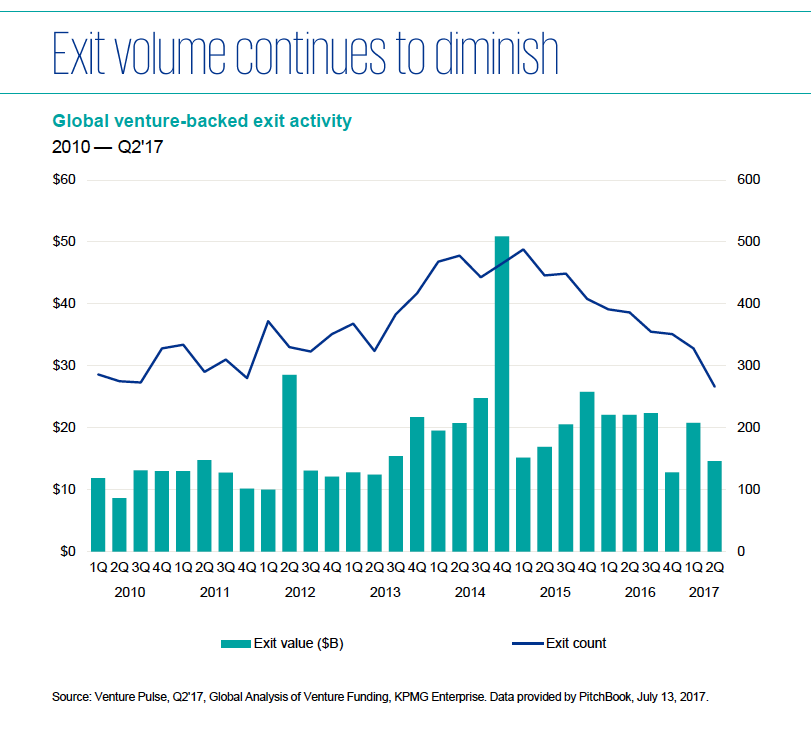

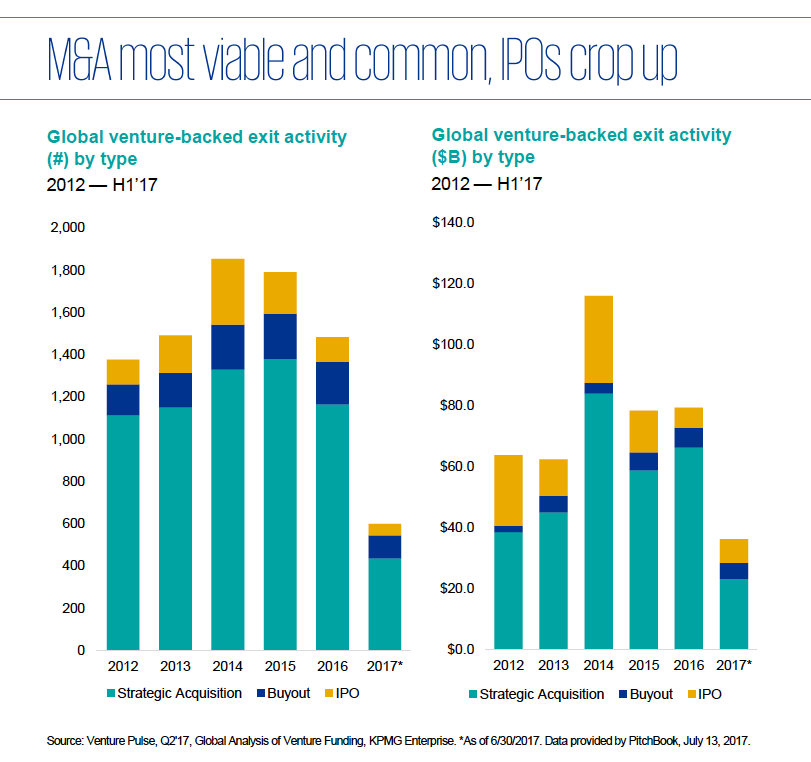

Headline numbers look good for global VC investment during the 2nd quarter of 2017 but the more interesting story is what’s going on underneath the surface.

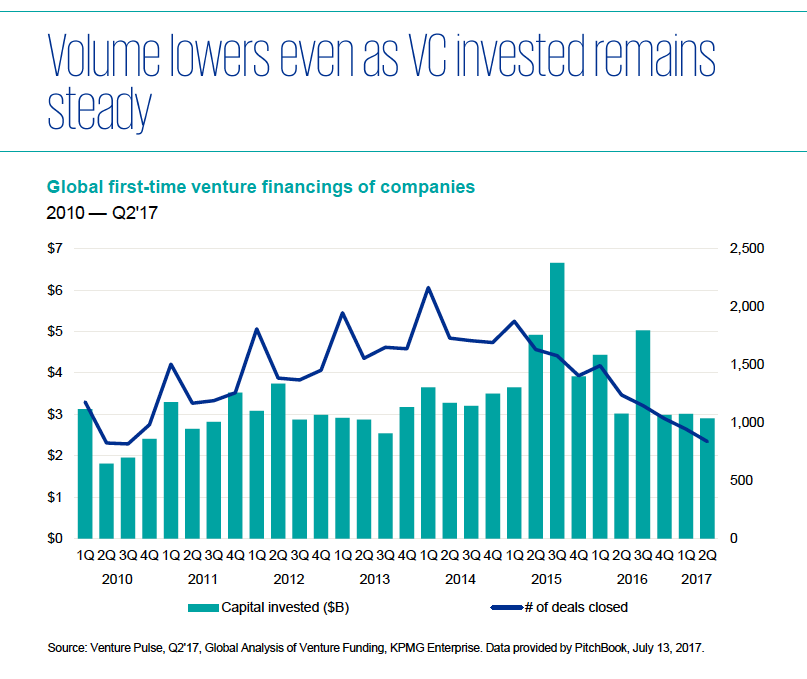

Digging into the details, below is the trend for first time investment activity (thanks KPMG + Pitchbook for crunching the numbers).

Even taking into account stealth rounds which have not been announced, the number of new companies has not been keeping up with the $ invested. And if you take the data at face value, the number of rounds is back to levels not seen in several years.

Instead, VC investors have been adding more to existing companies.

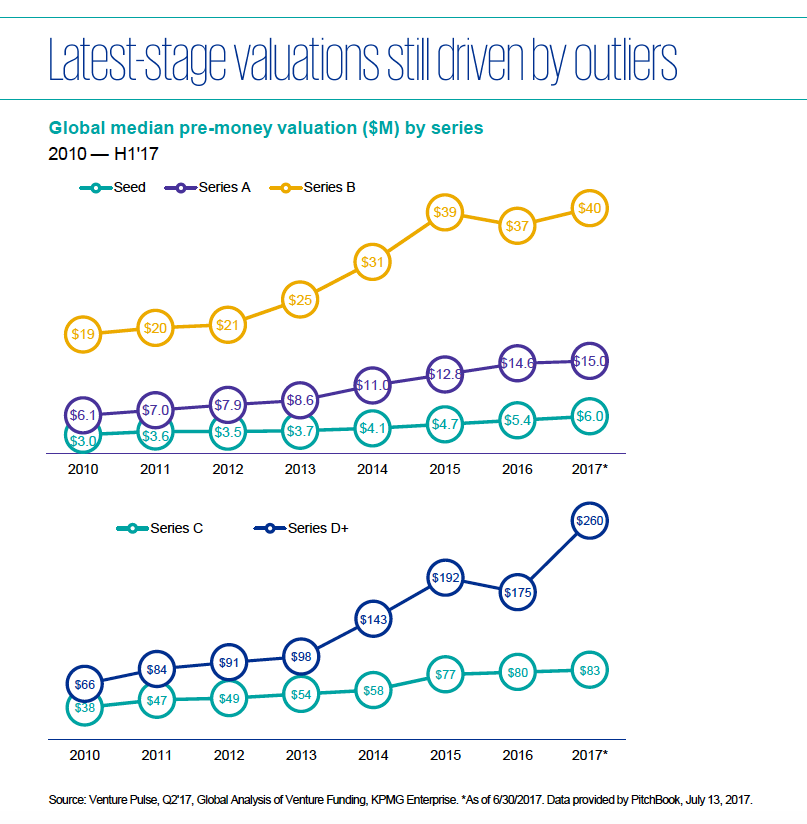

The increase in round size can be seen in most rounds, with the obvious outlier being the late stage Series D+. The above numbers are median, so the $40M figure likely understates the outliers.

The median pre-money valuations above tell a similar story:

fat rounds are back.

Why?

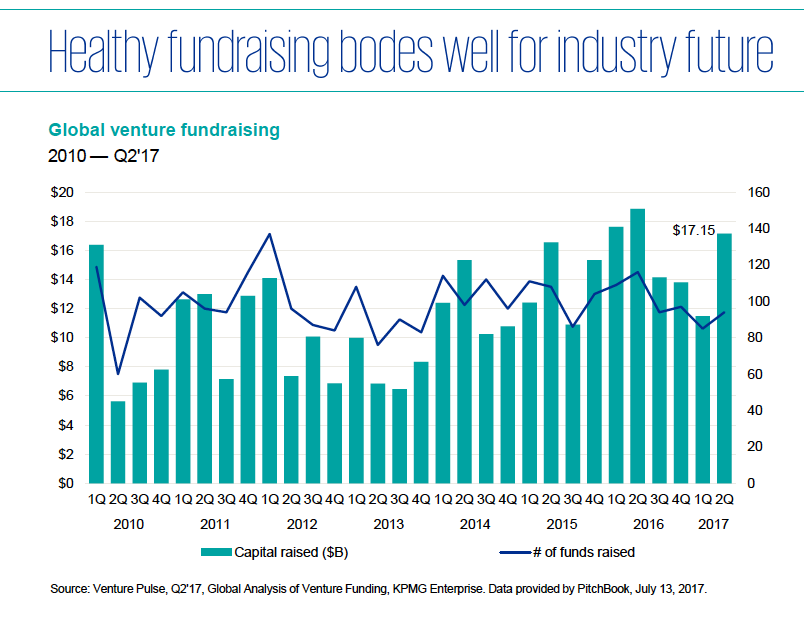

First, VC funds are cashed up.

VC funds are continuing to raise $ at an impressive rate. If you’re familiar with the timeline of how VC funds deploy capital, one guarantee is that managers will invest this money. They’re not going to give it back next year saying “I can’t find anything to do with it.” The capital will be around for, oh, about the next 10 years. VC funds will invest in something.

Second, corporate VC funds are having a big impact.

The rate of participation has been increasing steadily and in this last quarter they have been even more aggressive. Many of these funds are structured with external investors, including the headline grabbing Vision Fund. So like traditional VC funds, the capital should be around for several years (as contrasted with pure balance sheet investment from corporates which can be harder to predict over time).

Third, exit trends have been lukewarm for VC backed startups.

This has meant that late stage companies are staying private for longer. Those fat rounds are in some sense becoming short-term substitutes for M&A and IPO exits.

So there’s an interesting paradox.

On the one hand, corporate VCs are more active than ever before and investing aggressively in late stage fat rounds.

On the other hand, corporate M&A activity is not keeping pace.

Based on the lifecycle of capital raised, expect VC funds to continue investing in existing companies.

However, if market sentiment deteriorates, fat startups will become the victims of cap table recaps. There will be money, yes, but the terms will be harsh.

For startups, VC investors, and LP investors in VC funds, now would be a good time to remember the benefits of capital efficiency. For startups especially, make sure you understand the terms of rounds, not just the headline valuation.

Fat startup rounds are back. Let’s make sure we’re building healthy businesses because it sucks to be a fat, dead startup.

But think about it: When’s the last time you’ve download a new app that has truly transformed your life? It’s probably been awhile.

Yes, the average smartphone owner still uses apps. It’s just that we use the same five apps 80% of the time we spend on our phones. This makes it difficult for new apps to emerge and take over our phones to the point the average app loses 77% of its users within three days of being downloaded.

A Look Back

We used to have mainframes and terminals were the killer app back in the day. Then came along the client/server era and desktop application software (which ran on top of Windows). Up next, there was the web where the killer app was the browser and the webpage itself.

Which brought us to the app-filled mobile era — characterized by the lack or absence of desktop software and usually limited or no functionality on the web. Instagram didn’t have a web site until recently and there’s no (useful) web version of Candy Crush, for example.

It’s hard to imagine a world where apps are an afterthought. But as technology evolves and AI rises, we’re inching closer and closer to that reality.

The Post-App Era

We’re entering an era with no apps, no websites, no desktop software and no mainframe terminal.

For example, I was talking to a startup the other day. They don’t have an app.

You interact with it via chatbots in Facebook Messenger and other platforms. When you need to talk to a human, it jumps out to Skype.

The platform uses AI to keep track of interactions and it pings you on your Echo or Google Home to ask you for some input. It’s pretty cool stuff.

I asked the founder when they were planning to build an app. He told me that he figured they would have built an app by now, but they already had 50,000 daily active users and none of them have asked about an app — making it a low priority.

You wouldn’t have heard that five years ago. Or even a year ago.

Chatbots, Chatbots, Chatbots

According to Gartner, “smart agents” will facilitate 40% of all mobile interactions by 2020. Think Siri, Alexa, and Cortana — AI secretaries of sorts that learn more over time and can be customized to meet your specific needs.

Similarly, chatbots — which are already found on platforms like Facebook Messenger and Slack — will become a major communication medium for brands. Users of tomorrow (and today, really) will be able to pay their bills, shop for items, check the weather, and conduct research by interacting with these AI platforms.

It’s an exciting transition. Users won’t have to worry about hopping from app to app to app, nor will they have to worry about clogging their phones with apps they hardly use.

Whereas apps force users to behave in certain ways, chatbots, combined with AI and natural language processing, promise the ability to enable users to customize their experiences to their own preferences. The end result? A more efficient and enjoyable experience that adds more value to the user’s life.

Some people think venture capital is just fine and doesn’t need to change. Others want to turn it into a hyper liquid automated platform.

It’s time to call bullshit on both views.

Traditional venture capital needs to be transformed and the process will happen one person at a time.

I gave a presentation to a group of family office investors and corporate investors about the “Do’s and Don’ts of Venture Investing” earlier this year using martial arts training as a metaphor. It covers a lot of basics, with details here and here.

The discussion below starts with some of the traditional issues around risk and return, then moves on to ideas about how to transform venture capital.

At the black belt level, the emphasis shifts to higher level training, including awareness of self and the environment.

A typical mistake for a beginner in karate is to punch before stepping. This results in no power — as we learned in brown belt, strength starts from the bottom and flows upwards. It seems easy which why it’s actually difficult and in fact many people simply don’t even notice the mistake. Even with the incorrect technique, it still feels correct.

Getting the timing right in venture investing is similarly a challenge. The biggest mistake is to sell too early. The only thing worse than missing out on a billion dollar investment is being an early investor and then selling out to a new investor for a small profit and missing out on the much bigger gain. I know of one investor who came in very early into Alibaba only to sell soon just to get the money back because of concerns about risk. Whoops.

Of course, there are certain situations where it’s better to sell. This can happen especially when a wave of lemming behaviour overcomes investors to jump into a theme.

There’s no formula for getting the right timing to sell, but compared to all other investments venture capital is about long-term returns, so you should be thinking in terms of years and decades, not day trading.

The foundation of looking at the risk vs. return over time is to always evaluate decisions as if you were investing for the first time. In reality, that’s difficult in venture capital because of the knowledge built up over time after an initial investment and the overall lack of liquidity. Still, it helps to set the right framework. A more detached assessment of risk vs. return tends to lead away from binary all or nothing decisions and towards a more measured approach.

Of course, the process is not all about numbers. In fact, understanding the motivation of founders, other investors and of course your own goals is critical. If the company has been grinding it out for 10+ years and everyone is ready to move on, it may not matter that the best financial decision would be to continue for another 10 years because from a motivation perspective the journey has finished. Conversely, if the company has just received a lucrative M&A offer, this might be just the catalyst for a highly motivated founder to push for a more aggressive scaling up strategy and reject the early exit. Human inputs can be the most important factors when it comes to evaluating risk vs. return.

People are surrounded by external distractions. In addition, our minds are constantly creating internal distractions. This noise stops us from concentrating.

One description of traditional martial arts is “moving meditation”. Embedded in this description is the idea of having an empty mind. The first step is to navigate external distractions. The more difficult challenge is to manage internal distractions. Rather than trying to push the distractions out of our mind with mental energy, which is impossible, the training emphasizes acknowledging distractions and then being able to let go of them. Empty mind is not a static state of being, it is a dynamic process.

At first glance, it seems ridiculous that an empty mind would be an important skill for venture investing. Traditional wisdom suggest that experience, especially domain expertise, is necessary to be a successful venture investor.

The problem with experience is that it is actually one form of noise. The deeper the experience, the louder the noise. If you have 23 years of experience building microcomputers and some kid comes along with an idea for a personal computer, all your experience screams “impossible, no way this will work”. If you’ve spent all your career selling packaged software and someone suggest selling software for a monthly subscription, your instincts react immediately that customers simply wouldn’t trust software that they don’t own. If you’ve built billion dollar satellites and a young team proposes to create a network of cubesats, the first reaction is to treat it as a toy project. That’s the voice of experience speaking.

An empty mind allows even experienced venture investors to stay open to new opportunities. You can’t ignore your experience — those thoughts will always be there. Instead, acknowledge them, let them float away, and then let your empty mind stay open.

The common assumption is that martial arts focuses on fighting. But upon closer inspection, there’s a clear emphasis on peace by many traditional martial arts teachers. Fighting is the last option of traditional martial arts.

Many startup founders and venture investors make heavy use of war and sports metaphors — destroy the competition, hunt down customers, don’t be a loser.

Words and metaphors influence behaviour and actions. So by definition people being led by these words will be approaching the world with at zero sum perspective. For them to win, others have to lose. Zero sum thinking implies a lack of new value creation. If you believe that technology is supposed to create new value, not simply take value from others, then by definition these zero sum metaphors should be rejected.

Of course many others will continue to view the world from a zero sum perspective no matter what you do. Instead of wasting your energy on constantly fighting with them, focus instead on partners who you can trust.

Trust is much easier to build with aligned incentives and shared values. Aligned incentives alone may not be enough if the partner is going to find a way to cheat at the first opportunity. Shared values create great intentions but without aligned incentives, there may be no tangible outcomes. So it’s important to have both.

The right partners will help you reach your goals faster no matter what games others are playing.

Reaching a black belt level in traditional martial arts is not an end goal. It is more like reaching the starting line of the journey. At the higher levels, this learning includes the willingness to embrace paradox in many ways.

Traditional karate training obviously places a big emphasis on learning the basics. The only way to do this is through repetition so that it becomes automatic.

But the ultimate goal is not to become a clone of others from the past. Instead, every single karate student has a unique signature style. If you try to develop your signature style at the white belt level, you’ll just be fooling yourself. The style develops naturally over time without any extra effort through the process of repetition.

Learning from other investors about venture investing is a great shortcut. After all, nobody has the time to invent it all from nothing. To this day, I’m still reading Fred Wilson and Brad Feld on a regular basis.

You should absolutely learn from what venture investors are sharing both in public content and in private meetings.

But a copy and paste approach is unlikely to be optimal. Every venture investor’s background is unique. Each era is different. And it’s all path dependent. As an example, one of the big differences about our team at Fresco Capital compared to most other venture investors is our global cross-border approach. Most early stage investors are local and that works for them. We’ve chosen to be different precisely because of our background and experiences.

Instead of a copy and past approach, better to take the time to find trusted partners and work together with them. Co-create solutions that meet your unique needs. The ideal partners adds strengths to fill your gaps. This could be knowledge, network or other resources.

A key part of our global approach is working with local partners who are on the ground everyday in the local market. So just being global is not enough — working with these local partners is a key differentiation.

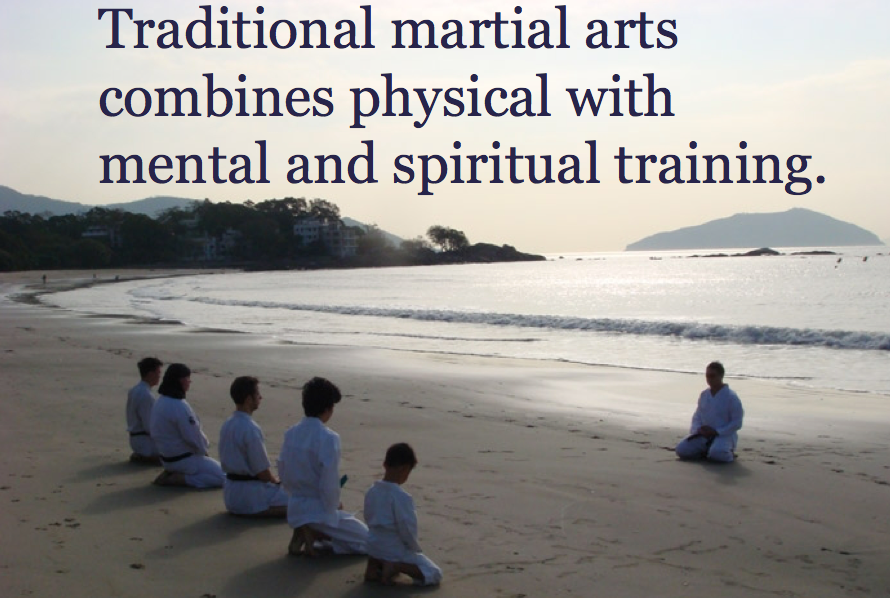

Martial arts starts with physical training. At a certain point, however, the mental and spiritual aspects of martial arts become more important than the physical training.

This doesn’t mean that the physical training is not important. The physical training is a gateway to reach the mental and spiritual benefits. Rather than being independent, they are integrated.

Venture investing starts with financial returns. This has to be the foundation. And many people do view venture investing as a box that takes money in and spits money out a few years later.

But this view overlooks the potential direct and indirect benefits beyond just the box of cash perspective. There can be positive effects on revenues, efficiency, and speed for related businesses. There may be harder to measure, but perhaps even more important, soft benefits such as upgraded team skills, improved innovation and entirely new business units which grow larger than existing businesses. Most importantly of all, all of this investment in innovation can, and should, be used to actually improve people’s lives.

It’s important to emphasize that these additional benefits are unlikely to materialize if financial returns don’t set a strong foundation. So start with the financial returns. But don’t limit your imagination to a box of cash. The ultimate potential is much bigger.

Venture capital investors are always questioning and challenging assumptions in other industries. It’s important that venture capital itself faces the same kinds of questions and challenges.

While industry insiders are looking for new ways to differentiate, a little extra push from external forces can only help accelerate the process.

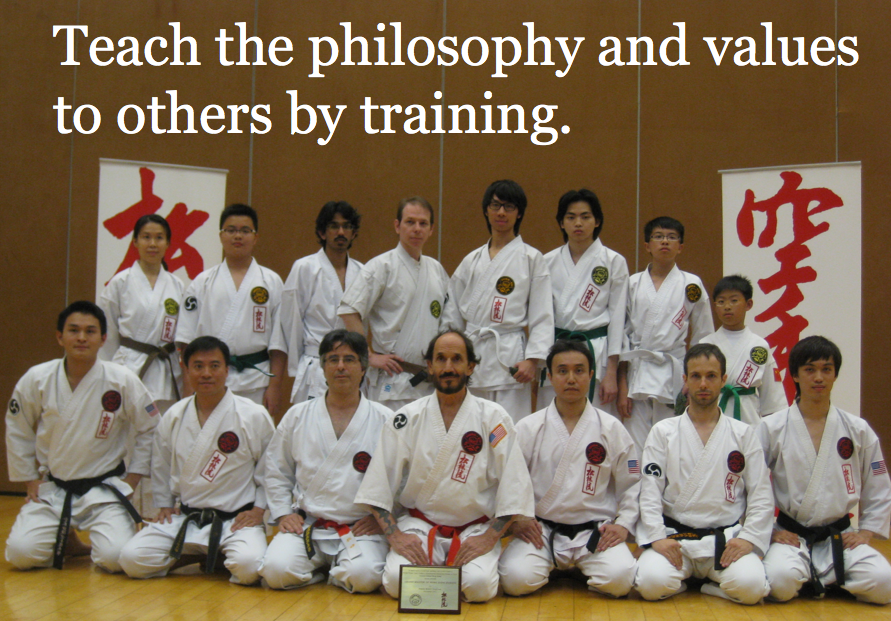

Ultimately, the best way to learn something is share it with others. In karate, this means training new students and then having them train students. This passes on the physical skills plus also the philosophy and values. None of this can be truly learned by reading a blog post or watching a video.

There is no substitute for person to person training.

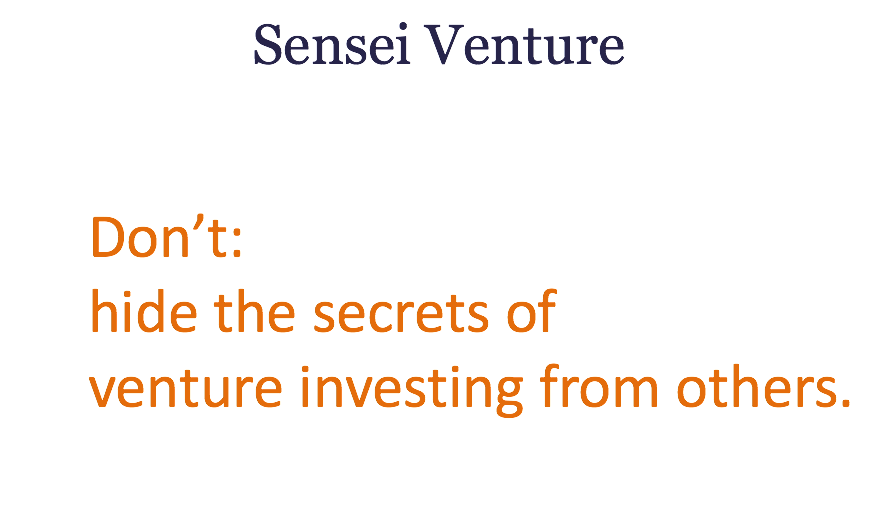

Historically, venture capital was a very secretive industry. Knowledge was not shared and venture capital firms put a lot of efforts into controlling information flow. This started to change in the past 15 years as the industry started to open up. Blogs and in person events have allowed people to learn more about venture investing. But the reality is that most of the activity is still behind closed doors.

True innovation requires an open ecosystem, and venture capital also needs to join this trend. So our view is that successful venture investors should not be trying to hide the secrets of investing from others.

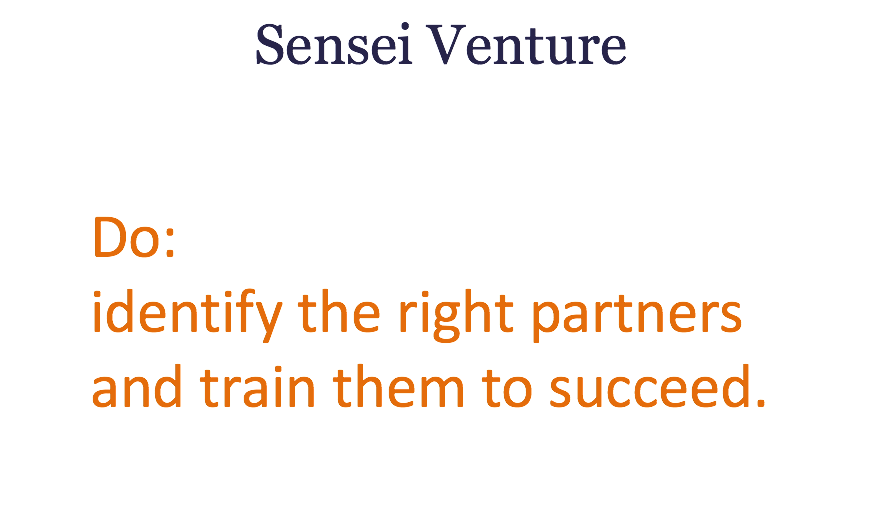

We believe there is tremendous value to be created in sharing knowledge about venture investing with others. More and more new investors are getting involved in venture capital. Without effective co-operation, that money may be completely wasted on bad investments.

Rather than hoping that other investors fail, we believe that the startup ecosystem desperately needs more high quality investors. This is not a zero sum game.

Of course, the challenge is to identify the right kinds of partners. There has to be an alignment of both values and incentives.

There’s a saying in karate: “a black belt is just a white belt who never gave up”. Learning to learn is the most important lesson of all. I’m still learning plenty about both karate and venture capital.

It’s this learning that is the secret power of how we can transform venture capital one person at a time.

It’s no secret, the widespread idea is that there’s a Series A gap in startup funding. You can easily raise a $1 million seed round and $100 million Series D, but somewhere in the middle things get a little dicey.

But as I’ve said before, there’s really no such thing as a Series A gap. Some companies just try to swing for the fences a little too soon and don’t drum up a lot of interest. Rather, they don’t focus intently on what they need to prove to secure the Series A or they focus on things that they think investors want to see.

The key to understanding the supposed gap, is that if your startup is really ready for a Series A, you can most assuredly raise money. You just need to be able to prove that your company has a repeatable and validated business model that can be scaled before walking into those meetings.

And this doesn’t mean you need to have tons of customers and millions in revenue by any means — a common misconception in today’s startup world. To raise a successful Series A round, start by proving the pipeline — and making financial projections based on it.

The Difference Between Seed and Series A

Seed money is supposed to help your startup figure out its business model. Seed is where you tell the story of what you are going to do. Series A, on the other hand, is more about making sure your business model works. You’ll also want to execute your story, telling people what you’ve done and what you’ll do next.

Let’s say you want to sell new coffee cups. During your seed, you should first focus on landing one or two landmark customers; maybe a few Starbucks locations that are proving to be loyal and consistently fill orders. When you’re pitching the Series A, show the investors that you can scale your business to every other Starbucks in the Palo Alto region and beyond, as well as Peets and other coffee shops — and the investor’s money is what stands between you and accomplishing that growth.

The Wrong Approach to Series A

Today, because of the emphasis on hitting a revenue target to signal a new round of funding, a lot of startups are guilty of growing their revenue linearly.

Imagine Starbucks is buying your new cups and you’re generating $50,000 ARR from that account. Then you decide to do non-core business model activities that pad your overall revenue. Maybe you consult for Peet’s Coffee and help out other startups in exchange for quick cash to keep the runway looking a little better.

Sure, all those extra funds are lumped into your total revenue. But let’s face it, that’s not the organic, scalable growth VCs are looking for.

You’d be much better off getting that one customer that fits your model, making some revenue off that sale, and then trying to get one more customer to show the pipeline potential. Focus on your core business, and a Series A will become that much easier.

Startups Love Revenue

It’s no secret that startups will chase revenue wherever it’s coming from. When you’re chasing a Series A, you’ll try to make whatever money you can to prove you have a business that generates revenue.

But let’s face it, not all revenue is created equal. This doesn’t mean revenue is necessarily bad, but time spent chasing after any revenue in sight can be a dangerous game in the early days of a startup.

There’s a common misunderstanding in the VC/startup world that a $1 million run rate means you’re ready for a Series A. In reality, there isn’t a benchmark that indicates the exact time you’re supposed to start raising money. Your run rate doesn’t matter as long as you can talk to investors about projected metrics.

How does that work? Start with your pipeline and your pipeline’s future. Show repeatability and show scalability. Show investors your funnel and the pipeline that goes into that funnel and tell them how you’re going to get there. That way, when you ask for lots of money to hire a certain number of salespeople and marketing folks, your request will be validated by the data up on the screen.

Whether you’re in a SaaS, B2B, or B2C business model, the same rules will still apply. So if it’s projecting growth in sales, the viral coefficient, or whatever else to show future scale, investors need to see the pipeline view of that story as validation before taking part in the round.

Key Takeaway

If you’re still trying to tell your company’s story, rather than actually using sales data to project growth, you’re likely better off waiting and raising a seed extension round.

How do you do that exactly? First, go back and see if your original investors are willing to go further in with you to bridge the company through to the next round; this may require you to give up more equity, but it will also be crucial to keeping the proverbial lights on. Also take time to look for firms that aren’t necessarily specializing in “Series A and above” funding — there is an abundance of seed stage investors out there looking to fill that gap.

Once you have an idea of how your business model will become scalable, use the extra time and cash to refine that story, validate the numbers, and make it real before pitching to Series A investors. This allows teams to focus less on generating non-core business model revenue, and more on securing a few necessary customers to project a data-backed pipeline. Once that happens, and you’re getting great feedback that shows the product or service is truly valued, it’ll finally be time to show later stage firms a clear vision of what you plan to do next.

Can you list the names of Silicon Valley companies that have succeeded in China? Can you list the names of foreign banks that have succeeded in China? There is only one name on both lists: Silicon Valley Bank (SVB).

SVB operates in China through a joint venture with Shanghai Pudong Development Bank (SPDB), and one of the senior leaders is Oscar Jazdowski, formally with the title of Deputy Head of Corporate Banking. I first met Oscar in 2013 while we were speaking on VC and startup ecosystem panel together and quickly realized that he wasn’t your typical banking executive. Seeing the success of the JV over the years, I recently had a chance to speak with Oscar and ask him to share some of the unique insights from the SVB experience in China.

Can you tell us some of the things that Silicon Valley Bank did before entering China as part of the preparation and how that preparation made an an impact on what happened after entering the market?

In 2005 we brought a delegation of about 10 top VCs from Sand Hill Road to China (Shanghai and Beijing). Folks like John Doerr from Kleiner Perkins, Don Valentine from Sequoia Capital, Dick Kramlich of NEA and other leaders of the VC community. For most of them, this was their first time in China. They all knew that China was growing and the likely future of technology. SVB set up a week of meetings with entrepreneurs and government officials and other related parties. Our goal was to get these US VCs to set up shop in China so that they would start investing in China and thereby build the ecosystem for us, into which we could lend to startups. It worked.

SVB also rented impressive office space in Xintandi, right in the center of Shanghai. We rented more space than we needed and built out a number of ‘guest’ offices which we offered to our US VC friends to use. That made their exploration and ultimate transition to China much, much easier because they did not have to go and look for office space in a foreign non-English (more so then) city. We made it easy for them to work out of our office, and that allowed us to stay close to them and see what they were beginning to do and explore in China. It helped us develop even closer relationships with them.

Silicon Valley Bank has been using a JV structure in China. What are the key factors that can make or break the results of a JV in China based on your direct experience and what you’ve observed in the market?

Always staff your JV with the most senior person you can from the parent company. In our case the first President of the JV Bank was SVB’s retiring CEO and Chairman, Ken Wilcox. By sending such a high level executive to China, you demonstrate (by action) to your joint venture partner, the regulators and to the government that you are 100% serious about China and that you are prepared to devote your absolute highest, most senior talent to make this JV successful. You also want those senior sponsors to stick around. This is very often the un-doing of JVs because the executive sponsors either get promoted to another part of the company or leave, thereby leaving the new JV bereft of a loving parent. The two key executives who brought our JV together are still around and even sit on our Board.

You need to have senior level backing, but that’s a given. The success of a JV is not determined at the executive suite, but in the trenches. You have to have a strong determined working group that gets things done. But the real success of a JV is defined at the working level. At the beginning of our JV, we would have monthly working committee meetings with our counterparts at SPDB in order to work on specific deals and issues.

Be aware that the two parties in a JV will have very different motivations. Understand what each party wants and then work to achieve that for them and have them do the same for you…even though each parties motivations might be polar opposites. As example, China and the JV bank is extremely important to Silicon Valley Bank from a long term perspective. If we are to remain the main bank globally to the technology/innovation/life science/ clean tech/ VC and PE industries, then we have to be in China. What is important to SPDB is that they can show the government that they formed a JV with this quirky bank from California and were able to stimulate and invigorate lending and financial backing of the Chinese innovation ecosystem. Two very different goals but both achievable so long as both parties understand what is important to the other and work towards these goals.

How did you find your JV partner in the first place, and what sort of due diligence process should foreign companies use when evaluating potential JV partners in China?

I wasn’t involved in the search for the JV partner myself but I spoke to many of my colleagues about the process at length. The story there is that we spoke to a number of Chinese banks, and we were looking for a partner who would be responsive, creative, risk taking, innovative, etc., and we found those qualities in SPDB. It was also chemistry, which is key in any JV. Our CFO connected very well with their CFO, who is now the President of SPDB, so that was very helpful in terms of building the relationship.

We also realized that when we entered a JV with a Chinese bank, we’re really entering it with the government because the government has to approve it and support it. So it was understanding that we needed to work with both the government and SPDB.

What about you personally? You didn’t live in China before and many foreigners who come to China don’t stay very long. What helped you make the transition?

When I first came to China, I was flattered, excited, and also a little bit apprehensive. I came over in late 2012 to meet the JV bank in Shanghai. When I went around the bank and met these individuals who were now all my colleagues, I asked them all the same question, “what brought you to SPD Silicon Valley Bank and why do you like working here?”

They basically all answered the same way, “we like the culture of the bank”. Culture in SVB is very important, and they answered in a way that an employee in our Seattle or Israel or Denver or San Francisco office would have answered. So as soon as they answered that way, I said to myself ‘wow, I know who you are’ because they answered exactly the same way that my other colleagues would from anywhere else in the world. That made me much more comfortable that I was coming into a culture that was very familiar to me because it was an SVB culture.

The other thing to succeed in any overseas environment, especially one as unique as China, is as an individual you have to be curious, like to get out of your comfort zone, like to take risk and that is my individual personal profile. Having said that, I knew by the answers from colleagues that I knew who I would be working with, so that reduced the risk factor dramatically.

On the topic of culture, one of the challenges that foreign companies have in China is finding, recruiting and retaining top talent. Can you talk about these issues?

On the corporate banking side, it’s relationship management and analysts, with an average age of late 20s to early 30s, bi-lingual, with many who finished universities in the US or UK, and then have worked with other international companies. We’ve got a big advantage with them because we are an innovation bank. That is clearly the drum beat in China today. We also have the words ‘Silicon Valley’ in our name, and those two words are very powerful and attract a lot of people.

We actually find that we attract a high calibre of talent because they’re intrigued by our bank. Our retention rate has been very good. In the case of losing people, we’ve lost people to people starting their own business or to join a VC firm. So we don’t lose people to other banks because they like the culture and the sector, but we can lose them to the lure of entrepreneurship or venture capital.

On the operation side, we are about to open our Beijing branch very soon subject to the final regulatory approval, and we had to hire more operations staff. We’ve hired more mature people who have been successful in their careers and see our bank as very intriguing and different. So there’s an appeal there for these more mature people who have worked in traditional banks for 15 years or more, and they’re saying that this is an interesting bank.

One of the things we’re criticized for is we put people through too many interviews. We also have written tests as well. We don’t do psycho-metrics type testing, it’s really based on understanding each individual as a person.

How do you think about the balance between the global culture of a company and the unique specifics of the local China market?

We put a lot of focus on culture. We focus on people who are creative and can enjoy an environment where everyone has a voice. So it’s a very similar culture to what is seen in our other locations. A lot of our employees in China like working for us and so our unique culture helps to differentiate. Of course, we’re very careful not to be arrogant about this and we recognize that we have to localize. We know many foreign companies have failed because they brought in their culture and they haven’t adapted and localized enough. It’s a balance, and that’s why the joint venture works well, because each side brings its DNA together. One thing I look back at now — had we had a local co-head, that may have been helpful to deal with local specifics. So even for us, it’s certainly possible we could have listened more to our local colleagues to understand the local marketplace.

Looking at localization in China, slogans are very popular. You have a new product, you give it a catchy name. You start a new year, and you have a slogan, like the ‘Golden Year’. Those sorts of slogans are important to employees for inspiration. It’s a very simple example but it’s important. We try and do things like sports days, hairy crab dinners, the regular Chinese New Year parties, and all the obvious things. We have social committees made up of Chinese employees who come up with ideas for building the culture.

In our early days, we would also ask the employees to put together skits, mini-plays, to our employees regarding things like ethics and customer relations. These would be funny skits but the underlying theme would be serious. The employees very much liked it. As we’ve scaled, there’s unfortunately not enough time to do it anymore, but it worked well.

Looking at the macro trends, are there specific themes that are particularly exciting?

The hot themes today are artificial intelligence, big data and virtual reality — those are hot everywhere, including China and Silicon Valley. People are noticing that China may be adopting virtual reality faster than other markets. Not just for entertainment and gaming, but also for enterprise applications.

The demographic shift in China is also driving a lot of themes as well. One venture firm is investing in amusement parks in shopping malls. Something we wouldn’t normally see but these are top tier VCs because families are going to shopping malls for entertainment.

In terms of business model, it’s now less about scale and more showing profitability over time. Not necessarily now, but at least the path to a profitable business model.

For the joint venture bank, what kind of company is interesting for you?

The same things that VC investors look for — a great team focusing on a large market with a defensible business, whether through intellectual property or some other unique edge, that can scale quickly. It doesn’t have to be deep technology.

For us, it’s also the quality of the investors and most importantly it’s management, management, management. You can have a great company and it can still fail with poor management. Our old CEO used to say to us that “cashflow doesn’t pay back the loan, people do”.

Most traditional banks are still focused on collateral, not people. What do you do differently?

It’s our focus on building relationships. We spend our time and energy deepening personal relationships.

Building a successful China JV starts with getting the people right. Oscar’s answers highlight that it is possible to have a strong and unique global company culture that also respectfully adapts to the local China market. While the specifics of each company are different, the lessons about finding the right partner and managing local talent are very relevant to all companies entering the China market.

As an American living abroad, I have been shielded from a lot of the insanity of this year’s election, but even sitting here in Tokyo, halfway across the world, the vitriol and frustration is palpable. Sure, the Presidential Election in the United States is always charged with emotion, but as almost anyone who has voted in multiple election cycles would agree, this year is particularly heated.

People have said harsh goodbyes to friends, unable to empathise with their choices. Families have lost touch, fearful of the difficult conversations that would ensue if the topic of politics were to be broached (I’m sad to say I speak from personal experience on that one). The very foundation of the Two Party System has been irrevocably damaged. The question of what it really means to be an American remains up for debate.

One thing is clear: Shit is broken. The world we lived in previously has changed. The American Dream used to be: work hard in school, get good grades, go to college, get a good job, find a wife who will take care of your house, buy a house, work hard, rise in the ranks, save your money, provide your children with a better life than you had, rinse, repeat. Sorry guys (yes, I mean guys), no can do.

For most people, that is no longer an option. College doesn’t guarantee you a job anymore (trust me, even a Harvard degree is worth less than it used to be). And even if it does get you a job, your job has probably started to be replaced by technology. Entire companies are being dismantled, so the idea of a long-term career at one company is rare. Most women don’t want to be just wives anymore, nor do they have to be. As the Great Financial Crisis taught us so painfully, houses don’t always go up in value, so they are not a safe investment anymore. Interest rates are zero, so saving doesn’t do you much good either. So… yeah, shit is broken. The promises we were sold have turned out to be empty, and it’s not really anyone’s fault, either. It just is.

Sure, we can try to put it all back together again. Go ahead and try. Even if that were possible, it still wouldn’t work again. Why, you ask? But why, can’t we just go back to the glory days? One word: technology. Technology has not only changed the world, but it has changed how fast the world changes. As our most recent Nobel Prize winner, Bob Dylan, so eloquently pointed out… “The times they are a’changing.” And they’re changing faster than ever before.

Nassim Nicholas Taleb, author of the Black Swan, wrote a fantastic book called Antifragile. I have a short attention span, so I’m not going to lie to you, I only read half of it. But the takeaway is this; Fragility is when you break something, and you cannot repair it. Resilience is when you break something, and it can return to its previous state. Antifragility (the best way to be), is when you break something, and it returns to an even better state, more powerful and strong than before it was broken.

I can only hope that part of what makes America great is that we are the definition of antifragile. We need to have faith in our ability to heal these rifts that emerged from the US election, to face the difficult conversations that must take place, and to emerge a stronger, more informed, more creative, and more antifragile nation than we were before.

Doing that, however, requires us to take a step back, to set aside our emotions, and to take a deep look at the incredibly valuable and previously unseen information revealed by this election. So let’s remove the emotion, take a quick look at the facts brought to light by this year’s Presidential Saga, and dedicate ourselves to building something better in its wake.

What have we learned?

Technology has forever changed how we, as individuals, make decisions.

We used to live in a world where information was difficult to access, and we relied on key institutions like the political parties, the media (newspapers, TV personalities), academic and religious institutions to tell us what we needed to know to make an informed decision.

Now, we get our information from the internet. Anyone can read about the candidates online, anyone can publish their opinion, anyone can state a “fact”, or share their emotional reactions. We have become infinite information consumers and producers.

As a result, it has been shown that our grip on the truth is loosening. Our willingness to hear arguments counter to our own beliefs is weakening. Our strength to overcome our own biases is diminishing.

The systems that have kept our world stable have not gotten the memo.

The key systems and infrastructure which shape our lives were all created in a time before technology existed. The idea that we would be meeting our mates on Tinder, sharing our momentary thoughts and emotions on Facebook, carpooling to work in a stranger’s car, or tracking our daily food intake and steps on an app were completely unfathomable at the time of their creation.

So, where does it all break down? Jobs. The systems that support the world as we know it can be broken down as follows: corporations that provide us with jobs, education which prepares us for those jobs, the government which protects those jobs and protects us if we don’t have jobs. (Ben Thompson writes brilliantly on this system here, if you’re interested in learning more how this system was created and why.)

As technology accelerates, companies are being forced to adapt to increase margins, productivity, and profits for investors. As a result, jobs are being automated. Because technology evolves faster than we can learn, or the education system can provide us with relevant skills, we are losing our jobs. People without jobs are angry, disappointed, disenchanted, and scared. Not a good equation for an election, or for anything for that matter.

It is up to us to rebuild those systems in a way that will last.

Technology is not a trend. It is not a sector. It is an inevitable force redefining the world in every way. This will not change, it will only accelerate. As outlined by the concept of singularity, the rate of change of technology will only get faster and faster. This unleashes unfathomable potential, but can also be disastrous if we don’t create a system that can keep up.

This brings us back to the concept of antifragility. We can’t simply repair our broken systems. We can’t simply aim for resilience. The only option is to imagine and re-build the world on a foundation that gains from change, and as a result, actually gets stronger over time.

Okay, fine. But what can we do about it now?

First, we have to stop wishing for “the way things were” and start taking a deep look at how we can start rebuilding a world that fits today’s reality. Because of technology, we are living in a world where we have unprecedented power as individuals. Yes, that is terrifying. But it’s also fucking awesome, because it means we all matter and we all have a role to play.

I continue to believe the only way for each of us to start making a difference is through education. Whether this is in K-12, universities, corporate training, online platforms, whatever. A few ideas:

Educate individuals on how to find, assess, and synthesize what is valid information and what is not.

Encourage empathy so that we have the discipline and intellectual strength to accommodate the views of others.

Raise awareness around our inherent biases so we know how to truly listen and learn.

Create ways that professionals can continually learn new skills, quickly and efficiently, so we can always find jobs.

Provide access to information about what jobs are available, and what we need to be get them.

The list goes on and on. Everyone needs to play their part, but first they need the tools that empower them to do so.

I am personally dedicated to doing whatever I can to help rebuild the systems that shape our world (not just America). That’s why we created Fresco Capital, where we are investing in the technology transforming these very sectors that need serious upgrades: education technology, work technology, digital healthcare. But that’s just one small part of a much bigger, more important picture of creating a new future.

So… let’s stop whining about this fucking disaster of an election and get started.